When you start looking at ways to save for a child's future, the conversation almost always lands on the UTMA account vs. 529 plan. The choice really comes down to a fundamental trade-off: do you want the ultimate spending flexibility a UTMA provides, or the powerful, education-focused tax advantages of a 529?

With a UTMA, you're giving an irrevocable gift that the child can use for anything once they come of age, but you lose control. A 529 plan, on the other hand, is built specifically for education, offering fantastic tax breaks while letting you, the parent, stay in the driver's seat.

UTMA vs. 529 Plan: Key Differences at a Glance

Getting to the right decision means really digging into how these two accounts work. They might both be ways to put money aside for a child, but they come from completely different philosophies. One is a versatile financial tool that legally belongs to the minor, while the other is a specialized instrument designed to fund education with some serious tax perks.

So, what matters more to you? Is it the tax-free growth for college that a 529 offers, or is it the all-purpose financial head start a UTMA can provide? It's also crucial to remember how each one is viewed when it's time to apply for financial aid, as that can make a huge difference for many families.

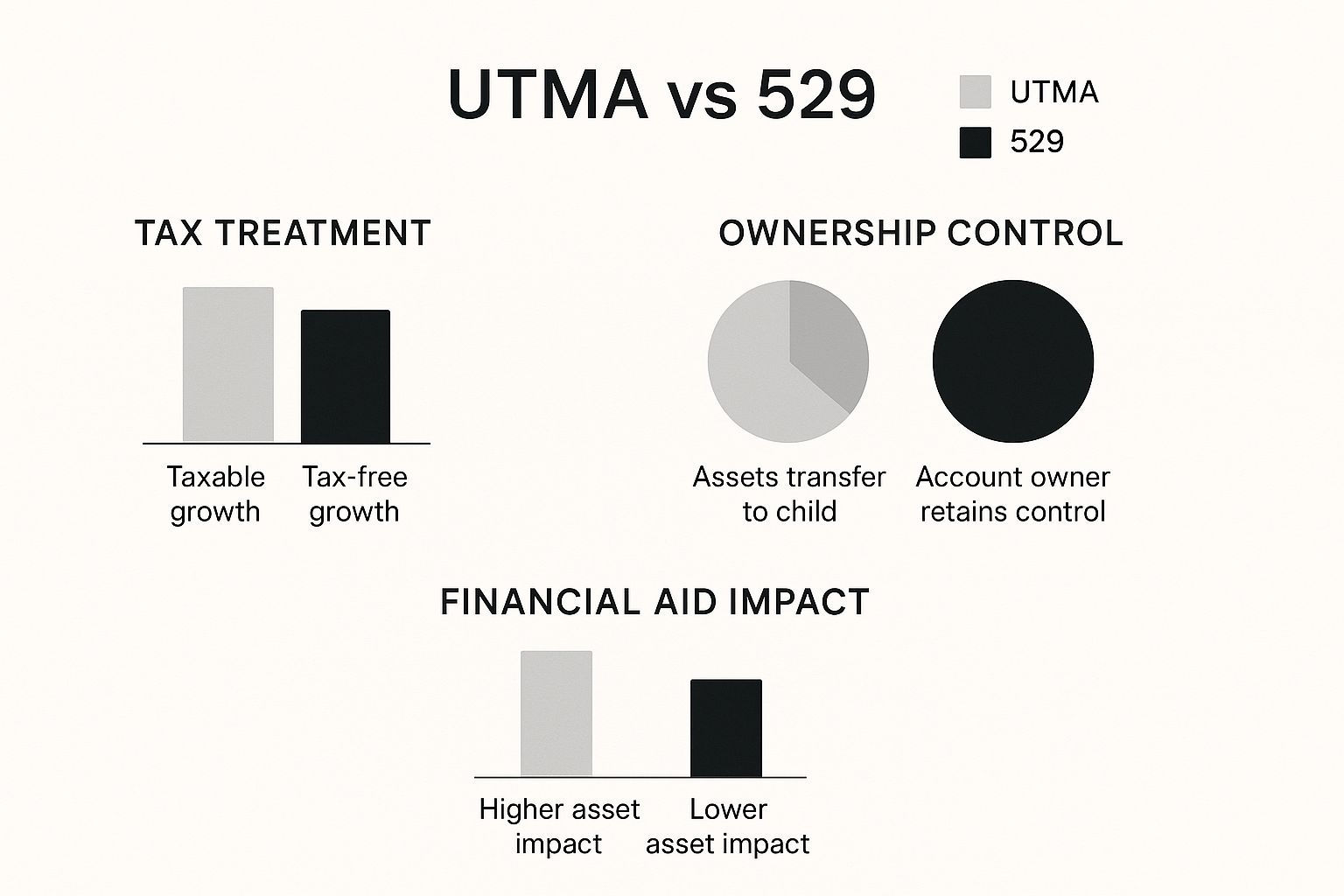

This image lays out the most important distinctions you'll need to consider.

As you can see, 529 plans are the winner for tax-free growth and parental control, but a UTMA account gives you nearly endless investment freedom—though it can have a much bigger impact on financial aid eligibility.

Of course, these aren't the only two options out there. To get a fuller picture, it's smart to see how they stack up against other savings tools. If you're weighing college savings against your own retirement goals, our guide comparing the Roth IRA vs. 529 can offer some valuable perspective.

Quick Comparison: UTMA vs. 529 Plan Features

To make things even clearer, let's break down the core features of each account side-by-side. This table gives you a quick, at-a-glance look at the most important differences.

| Feature | UTMA Account | 529 Plan |

|---|---|---|

| Primary Use | Any expense that benefits the child | Qualified education expenses |

| Asset Control | Irrevocable gift; child gets full control at 18 or 21 | Account owner (usually the parent) keeps full control |

| Tax Benefits | Earnings are subject to the "kiddie tax" | Tax-free growth and withdrawals for qualified expenses |

| Financial Aid Impact | High impact (counted as a student asset) | Low impact (counted as a parental asset) |

| Investment Options | Nearly unlimited (stocks, bonds, funds, etc.) | Limited to the specific plan's investment portfolios |

| Beneficiary Change | Cannot be changed | Can be changed to another eligible family member |

Thinking through these points should give you a solid foundation for deciding which path is the right fit for your family’s goals and financial situation. Each account has its place, and the best choice depends entirely on your priorities.

Flexibility and Taxes: Where the Real Differences Emerge

When you're looking at a UTMA account vs. a 529 plan, the conversation quickly moves past just saving money and into two critical areas: how you can use the money and what the tax bill looks like. This is where the two accounts really part ways. One gives you incredible freedom, while the other offers potent, laser-focused tax benefits for education.

A UTMA account is almost like a general-purpose savings fund for a child. Since the money is an irrevocable gift to them, it can be used for anything that directly benefits the minor. Think bigger than just college—this could be paying for a spot at a competitive summer camp, buying their first car, or even covering unexpected medical costs. The versatility is its biggest strength, creating a financial safety net for all sorts of life events, not just school.

How UTMA Accounts Are Taxed

That flexibility isn't free, though. The trade-off comes at tax time. Unlike a 529 plan, the earnings inside a UTMA account aren't tax-sheltered. Instead, they fall under what are known as the "kiddie tax" rules.

It generally works like this:

- The first small slice of unearned income each year is tax-free.

- The next slice is taxed at the child's own, typically much lower, tax rate.

- But once the earnings exceed a certain annual threshold, they get taxed at the parents' higher marginal rate.

This means a large, successful UTMA account can create a noticeable tax drag each year, which might eat into your long-term returns.

The 529 Plan: A Tax-Smart Tool for Education

This is where the 529 plan shines. It was built from the ground up for one thing: saving for education. Its tax structure is its superpower. While a UTMA offers broad flexibility, as a resource on how a UTMA compares to a 529 plan from SmartAsset.com explains, the core advantage of a 529 is that earnings grow tax-deferred and can be withdrawn completely tax-free for qualified education expenses.

That tax-free growth and withdrawal feature is a huge deal. It means every penny of investment growth can go straight toward tuition, books, or housing, untouched by federal and, in most cases, state income taxes.

The Bottom Line: The 529 plan is built to maximize your savings specifically for education by using powerful tax breaks. The UTMA account offers unmatched flexibility for any expense that benefits the child but requires you to pay taxes on the investment gains along the way.

The definition of "qualified expenses" for a 529 has also gotten much broader over the years, which adds to its appeal. It now covers:

- College costs like tuition, fees, books, and room and board.

- Up to $10,000 annually for K-12 private school tuition.

- Up to a $10,000 lifetime limit for paying down qualified student loans.

- Costs for certain apprenticeship programs.

There's a catch, of course. If you pull money out for something that isn't a qualified expense, the earnings portion of that withdrawal gets hit with a double whammy: ordinary income tax plus a 10% federal penalty. This penalty is a strong motivator to keep the funds dedicated to education. Your choice really boils down to what you're trying to achieve: tax-optimized funding for school or a flexible financial gift for your child's future.

How Each Account Impacts Financial Aid Eligibility

When you're comparing a UTMA account to a 529 plan, it's easy to get lost in the details of investment options and tax benefits. But one of the most critical, and often overlooked, factors is how each account affects your child's chances of receiving financial aid. The way federal aid formulas view these two accounts is night and day, and your choice can drastically change the amount of need-based aid your child qualifies for later on.

The entire difference boils down to one simple question: Who legally owns the money? Financial aid applications like the Free Application for Federal Student Aid (FAFSA) look closely at whether an asset belongs to the parent or the student, and that distinction determines how heavily it's counted against you.

UTMA Accounts and Financial Aid

Here’s the catch with UTMA accounts: legally, that money belongs to your child. Because of this, it must be reported as a student asset on the FAFSA. This is a big deal because student assets are assessed at a much higher rate than parental assets, which can seriously diminish financial aid eligibility.

Under the FAFSA formula, 20% to 25% of a UTMA account's value is considered available to pay for college costs. This means your child’s eligibility for need-based aid is reduced by that same amount. If you'd like to dig deeper into the numbers, financial experts at Western & Southern offer a great breakdown of how UTMA and 529 assets are assessed differently.

Simply put, a healthy UTMA balance can become a major obstacle for families banking on grants or other forms of need-based aid to make college affordable.

The 529 Plan Advantage

This is where the 529 plan really shines. When a 529 plan is owned by a parent, it's treated as a parental asset. The FAFSA formula is far more lenient with parental assets, assessing them at a maximum rate of just 5.64%.

This dramatically lower assessment rate means that the money you've saved in a parent-owned 529 has a much smaller dent on your child's financial aid package. You, the parent, keep control over the account, and the funds are counted far less heavily against your family.

Key Insight: The owner of the account changes everything. A UTMA is considered the student's property and gets hit hard in aid calculations. A parent-owned 529 is a parental asset and has a minimal impact.

Let's put this into perspective with a real-world example.

Scenario: A $50,000 Savings Fund

- $50,000 in a UTMA Account: Assessed at 20%, this would increase the student's Expected Family Contribution (EFC) by $10,000. That's $10,000 less in potential need-based aid.

- $50,000 in a Parent-Owned 529 Plan: Assessed at 5.64%, this would increase the family's EFC by only $2,820.

In this scenario, just by choosing a 529 plan over a UTMA, the family preserves more than $7,000 in potential financial aid eligibility for a single year. If qualifying for need-based aid is a cornerstone of your college funding strategy, the 529 plan presents a clear and significant advantage.

Who Really Owns the Money? A Deep Dive into Asset Control

When you're weighing a UTMA against a 529 plan, one question towers above the rest: who actually controls the money? This isn't just a technicality; it's the core difference that shapes how these accounts work and what they can achieve for your child's future. The answer reveals two fundamentally different philosophies on gifting and saving.

With a UTMA account, any money you deposit is legally an irrevocable gift. That's a crucial point. Once it's in, it belongs to the child, period. You, as the custodian, are simply the manager of their money, and you're legally bound to use it only for their direct benefit. You can't change your mind and take it back.

This clear-cut ownership rule sets the stage for the single most important event in the life of a UTMA account.

The UTMA's Built-In Hand-Off

The defining feature—and for many, the biggest risk—of a UTMA is the mandatory transfer of control. When the child reaches the age of majority in their state, which is typically 18 or 21, the account is theirs. All of it. No strings attached.

They get full, unrestricted access to the entire sum. Whether they spend it on tuition, a down payment on a house, a lavish trip to Europe, or a questionable startup idea is entirely up to them. Your say in the matter is officially over. This potential loss of control is a serious consideration for anyone who wants to ensure the money is used wisely.

529 Plans: Where You Stay in the Driver's Seat

This is where 529 plans offer a completely different experience. In a 529, the account owner—usually the parent or grandparent who opened it—retains full control forever. The child is only the beneficiary; they never legally own the assets, and control never automatically transfers to them.

This ongoing control gives you a level of flexibility that UTMAs simply can't match. As the account owner, you call all the shots. You decide:

- When to take money out for qualified expenses.

- How the funds are invested.

- If you need to change the beneficiary to another family member—say, if the first child gets a full scholarship.

Key Takeaway: In the UTMA vs. 529 debate, control is often the deciding factor. Think of a UTMA as a gift with a non-negotiable hand-off date. A 529, on the other hand, lets you act as the financial quarterback for the life of the account, ready to pivot as your family's circumstances evolve.

Comparing Investment Options and Strategies

When you get down to the brass tacks of investing, the choice between a UTMA account and a 529 plan often boils down to one simple question: how hands-on do you want to be? One path gives you total freedom, while the other offers a guided, almost "set-it-and-forget-it" experience.

A UTMA account is essentially a standard brokerage account in your child's name, and you're the one in the driver's seat. As the custodian, you have a massive amount of freedom. You can invest in individual stocks, bonds, mutual funds, ETFs—even alternative assets if that’s your style.

This flexibility is a huge plus for experienced investors who want to actively manage their child's portfolio or teach them about specific companies. You can build a completely custom portfolio from the ground up. For a deeper dive into building a child's portfolio with specific assets, you can check out our guide on investing for minors.

529 Plan Investments: A More Structured Path

On the other side of the coin, 529 plans are designed for simplicity. You aren't picking individual stocks or trying to time the market. Instead, you choose from a curated menu of investment portfolios managed by the state's plan administrator.

These investment options are built to be straightforward and typically include:

- Age-Based Portfolios: This is the most popular choice. The portfolio starts out aggressive when your child is young and automatically becomes more conservative as they get closer to college age.

- Static Portfolios: These maintain a fixed allocation of stocks and bonds based on a set risk level you choose, from conservative to aggressive.

- Individual Portfolios: Some plans give you a bit more control, letting you build a custom mix from a limited list of underlying mutual funds.

This structured approach is perfect for parents who don't have the time or expertise to manage a portfolio and just want a simple, effective way to save for education.

Key Difference: With a UTMA, you have near-total investment freedom for a hands-on strategy. A 529 plan offers simplified, pre-built investment portfolios designed for a long-term, hands-off approach.

Since their introduction in 1996, 529 plans have become the go-to vehicle for education savings. Every state and Washington, D.C., now sponsors at least one plan, and by 2024, they held hundreds of billions in assets nationwide. This incredible growth, as detailed by resources like CFNC.org, is largely due to their ease of use.

Ultimately, your decision comes down to what fits your style: the complete control and responsibility of a UTMA, or the guided simplicity of a 529.

Which Account Is Right for Your Family?

Deciding between a UTMA account and a 529 plan can feel a bit theoretical. The best way to make sense of it all is to see how these accounts work in the real world. Honestly, the right choice comes down to your family's specific situation, your financial goals, and what you’re trying to build for your child’s future.

Let's walk through a few common scenarios to see how the unique strengths of each account play out.

By putting ourselves in the shoes of different families, you'll get a much clearer picture of which path makes the most sense for you.

The College-Focused Family

First, picture a family whose number one priority is paying for college. They’re banking on their child pursuing higher education and want to make their savings go as far as possible. For them, tax advantages and protecting financial aid eligibility are the most important factors.

In this scenario, the 529 plan is the hands-down winner. The tax-free growth and tax-free withdrawals for qualified education expenses are a massive benefit. On top of that, a 529 is considered a parental asset, which means it has a much smaller impact on financial aid calculations. This helps preserve the child’s chances of getting need-based scholarships and grants.

The Flexibility Seekers

Now, let's think about a different family. They want to give their child a solid financial head start, but they aren't convinced it will all go toward a traditional four-year degree. Maybe the money will be used for a down payment on a first home, to launch a business, or even to fund travel during a gap year.

This family would almost certainly gravitate toward a UTMA account. While it doesn’t have the tax perks of a 529 and can be a negative for financial aid, the UTMA’s core appeal is its incredible flexibility. Once the child reaches the age of majority, the money is theirs to use for any purpose that benefits them, providing a financial launching pad for whatever life throws their way.

Key Insight: Your primary goal really dictates the right account. If the money is earmarked strictly for education, the 529 plan’s tax and financial aid advantages are tough to beat. But if you're aiming for ultimate flexibility to cover any major life event, the UTMA is the better tool for the job.

The Estate-Planning Grandparents

Finally, consider grandparents looking to pass down a portion of their wealth in a thoughtful, structured way. Their goal is twofold: contribute to their grandchild's future while also being smart about their own estate.

They have a couple of great options here. They could use a 529 plan to make a significant, tax-advantaged gift for education, even front-loading five years' worth of gift tax exclusions into a single contribution. Alternatively, a UTMA provides a simple, direct way to make an irrevocable gift that the grandchild will control down the road.

Answering Your Top UTMA vs. 529 Questions

When you start digging into the details of UTMA and 529 plans, a lot of "what-if" questions pop up. It’s one thing to understand the basics, but it's the real-world scenarios that really matter for your family's financial future. Getting these answers straight is key to planning with confidence.

Let's walk through three of the most common questions I hear from families trying to choose between these powerful savings accounts.

What Happens to a 529 Plan if My Child Doesn't Go to College?

This is easily the biggest fear for parents saving in a 529. The good news is, you're not stuck. If your child decides college isn't for them, you have several great options, and you won't lose all your hard-earned savings.

Here’s what you can do:

- Change the Beneficiary: You can simply switch the beneficiary to another qualified family member. This could be a younger sibling, a cousin, a grandchild, or even yourself if you decide to go back to school. The best part? There are no tax consequences for making this change.

- Rollover to a Roth IRA: Thanks to a relatively new rule, you can roll unused 529 funds directly into the beneficiary's Roth IRA, completely tax- and penalty-free. There are a few guardrails: the 529 account must be at least 15 years old, and there's a lifetime rollover limit of $35,000 per beneficiary.

- Make a Non-Qualified Withdrawal: You always have the option to just take the money out for any reason. If you do, you'll owe ordinary income tax plus a 10% federal penalty, but—and this is a crucial point—only on the earnings. Your original contributions come back to you tax-free.

Can I Convert a UTMA Account to a 529 Plan?

Yes, you absolutely can, and it's a common strategy. The process involves selling the assets held in the UTMA account and then using that cash to open a specific type of 529, sometimes called a custodial 529.

One Critical Catch: Moving the money into a 529 gives you all the great tax benefits and better financial aid treatment. However, it doesn't change the fundamental ownership rule of the UTMA. The money still legally belongs to the child and must be turned over to them when they reach the age of majority (usually 18 or 21).

So while you gain tax-advantaged growth, you don't gain the long-term control that a standard, parent-owned 529 plan offers.

Are There Contribution Limits for These Accounts?

The contribution rules for UTMAs and 529s are quite different. Neither has an annual limit set by the IRS, but both are tied to the annual gift tax exclusion rules.

For 2024, this means you can contribute up to $18,000 per person (or $36,000 as a married couple) to either type of account without having to file a gift tax return.

However, 529 plans have a special feature called "superfunding." This allows you to front-load five years' worth of gifts at one time—that's up to $90,000 from an individual—without triggering the gift tax. It's a powerful way to get a lot of money working for you early on.

On top of that, 529 plans also have aggregate contribution limits, which are set by each state and are often very generous, sometimes over $500,000 per beneficiary. UTMA accounts have no such lifetime limits because they are simply considered irrevocable gifts to the minor.

A Quick Heads-Up

Before we dive in, let's get one thing straight: this article is purely for informational and educational purposes. Think of it as a guide to help you understand your options, not as a substitute for professional financial, legal, or tax advice.

We are not financial advisors. The world of investing and saving—especially when it comes to planning for a child's future—is complex and deeply personal. What works for one family might not be the right fit for another.

Because of this, we strongly encourage you to chat with a qualified professional. A financial advisor can sit down with you, look at your specific situation, and help you map out a strategy that aligns with your unique goals before you decide between a UTMA account and a 529 plan.

Disclaimer: The content provided in this article is for informational purposes only and does not constitute financial advice. We are not a financial advisor. The information presented is not intended to be a substitute for professional financial, legal, or tax advice. You should consult with a qualified professional before making any financial decisions.