Give your child a $1M head start-tax-free

Get our free guide—no finance jargon, just simple steps.

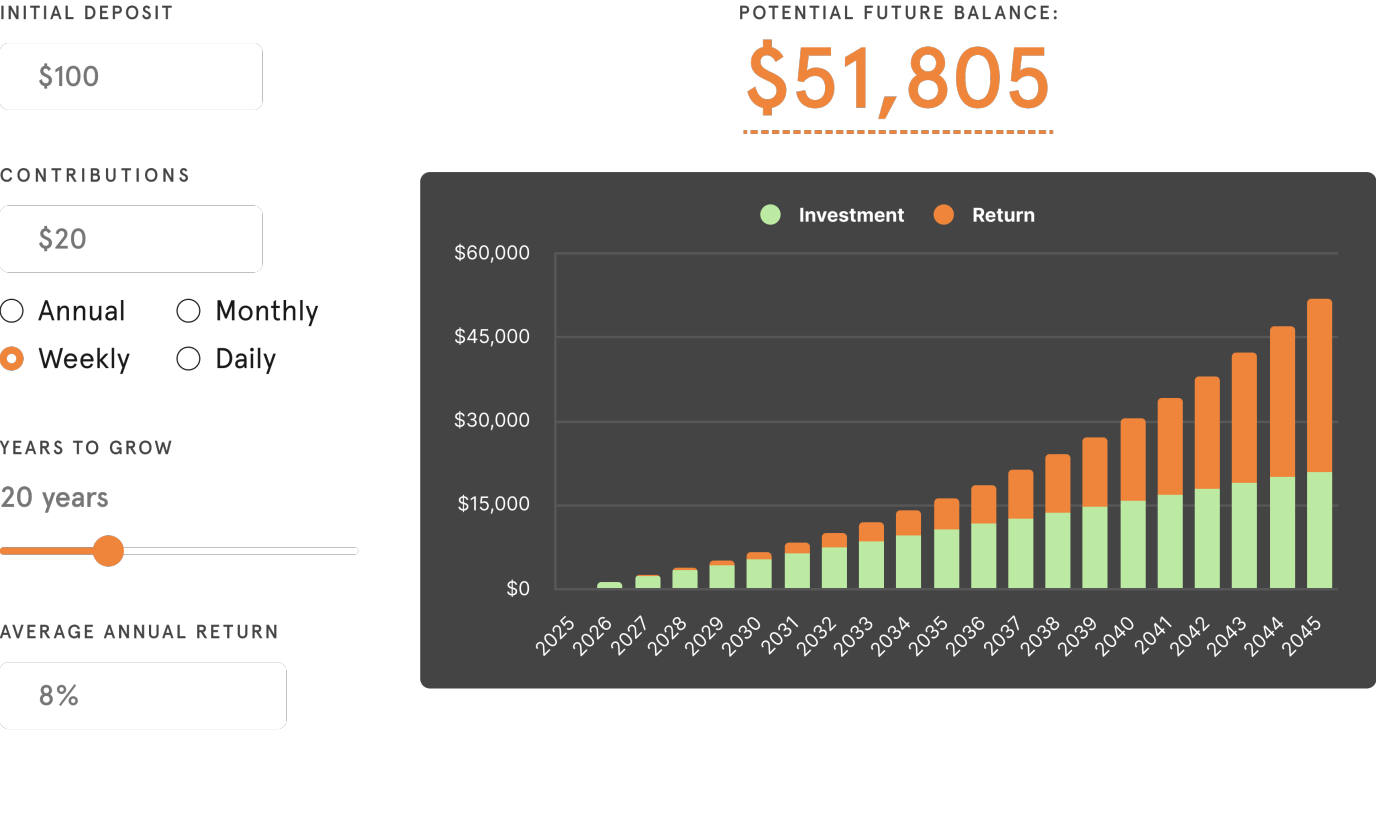

Power of Compounding

See your child’s potential

How much could your kid’s Roth IRA grow? Try our calculator.

The chart shows an estimate of how much an investment could grow over time based on the initial deposit, contribution schedule, time horizon,

and interest rate specified. Changes in those variables can affect theå outcome. Reset the calculator using different figures to show different

scenarios. Results do not predict the investment performance of any Acorns portfolio and do not take into consideration economic or market

factors which can impact performance.

Everything you need to get started

LEARNING

Learn from the experts

Can a 5-Year-Old Have a Roth IRA?

From Lemonade Stands to Roth IRAs

Roth IRA vs. 529 Plan: Which Wins for Kids?

About myself

Helping your child shine

I’m Naxin Wang, a mom and the founder of Obento Health. After years leading data and product teams at Google and Verily, I learned how small, steady actions can create meaningful change. When I discovered how a Roth IRA for kids can secure a child’s future, I knew I had to share this with other parents who dream of giving their children every opportunity to shine.

Frequently asked questions

Yes, absolutely. It is perfectly legal and encouraged by the IRS for a minor to have a Custodial Roth IRA, provided they have earned income. The key is the "custodial" part: an adult (typically a parent or guardian) opens and manages the account on behalf of the child until they reach the age of majority (usually 18 or 21, depending on the state). This allows your child to harness the incredible power of tax-free compound growth over a 50+ year time horizon, giving them a massive head start on their financial future.

This is the golden rule of a Roth IRA for kids: the contribution must be funded by the child's legitimate earned income. The IRS defines earned income as money received for work performed. This includes:

- W-2 Income: Wages, salaries, or tips from a formal job (e.g., working at a local store, summer camp, or restaurant).

- Self-Employment Income (1099): Money earned from a side hustle or small business where the child is providing a service or selling a product (e.g., babysitting, mowing lawns, dog walking, tutoring, selling crafts online, or designing websites).

Important: Unearned income, such as gifts, allowances, or investment earnings, does not count toward the Roth IRA contribution limit. The child must have actively worked to earn the money.

Maintaining clear records is essential for an IRS-compliant Roth IRA. The method of proof depends on the type of income:

- For W-2 Income: The W-2 form provided by the employer is the official documentation.

- For Self-Employment Income: You must keep detailed, contemporaneous records. This includes:

- Invoices or Receipts: Documentation showing the service provided, the date, and the amount paid.

- Logbooks: A simple log detailing the work performed, the hours worked, and the payment received.

- Bank Records: Deposits that correspond to the work performed.

While the child may not need to file a tax return if their income is below the standard deduction, having these records is crucial to prove to the IRS that the contribution is based on legitimate earned income, which is the foundation of the custodial Roth IRA.

Theoretically, yes, if they have legitimate earned income. There is no minimum age requirement for a Roth IRA. However, the requirement for earned income is the limiting factor. For a toddler, this would typically involve modeling, acting, or being paid for work in a family business. If a toddler is paid a reasonable wage for services rendered, and that income is properly documented, they are eligible. For most families, the Roth IRA becomes a practical option when the child is old enough to perform common tasks like babysitting, lawn care, or other self-employment activities.

The annual contribution limit for a custodial Roth IRA is the lesser of two amounts:

- The child's total earned income for the year.

- The annual IRS limit for Roth IRAs (which is $7,000 for 2024).

For example, if your child earns $1,500 from a summer job, the maximum contribution is $1,500. If they earn $10,000, the maximum contribution is $7,000 (for 2024). This limit is subject to change by the IRS each year.

Generally, a Roth IRA is one of the most favorable assets for financial aid purposes.

- FAFSA/CSS Profile: Retirement accounts, including Roth IRAs, are typically not counted as an asset in the federal financial aid calculation (FAFSA). This means the money saved in the Roth IRA will not negatively impact your child's eligibility for need-based aid.

- Withdrawals: If the child were to withdraw the contributions (not the earnings) for college expenses, those withdrawals are tax-free and penalty-free, and they are generally not counted as income for financial aid purposes.

This makes the Roth IRA a powerful, dual-purpose vehicle: a tax-free retirement fund that also protects assets from financial aid calculations.

Yes, but with a crucial caveat. Only the child's earned income can be contributed to the Roth IRA. However, the money used to make the contribution does not have to come directly from the child's paycheck.

- The Rule: A grandparent (or parent) can gift the child money, and the child can then use that gifted money to make the Roth IRA contribution, as long as the contribution amount does not exceed the child's total earned income for the year.

- The Action: The grandparent gives the child $2,000 as a gift. The child earned $2,500 from a job. The child can use the $2,000 gift to fund the Roth IRA contribution because it is less than their $2,500 earned income limit.

This is a fantastic way for grandparents to support their grandchild's financial future without violating the earned income rule.

Both are excellent tools, but they serve different primary goals and offer distinct advantages:

| Feature | Custodial Roth IRA | College Savings Plan |

|---|---|---|

| Primary Goal | Tax-Free Retirement Savings | Tax-Advantaged College Savings |

| Tax Benefit | Contributions and all growth are tax-free upon qualified withdrawal in retirement. | Contributions grow tax-free, and withdrawals are tax-free if used for qualified education expenses. |

| Flexibility | High. Contributions (but not earnings) can be withdrawn tax- and penalty-free at any time for any reason. | Limited. Non-qualified withdrawals of earnings are subject to income tax and a % penalty. |

| Financial Aid | Favorable. Generally not counted as an asset in FAFSA calculations. | Less Favorable. Counts as a parental asset, which can slightly reduce financial aid eligibility. |

| What if they don't go to college? | The money remains for retirement, or can be used for a first home purchase. | Non-qualified withdrawals incur tax and penalty. Can be rolled over to a Roth IRA (up to $k lifetime limit, subject to rules). |

RothIRA.kids' perspective: The Roth IRA is the superior choice for a child's long-term wealth creation because of its unmatched flexibility and the power of tax-free growth for 50+ years. It's a "no-regrets" account: if they go to college, the contributions can be used; if they don't, they have a massive, tax-free retirement fund. The 529 is a great supplement for college, but the Roth IRA is the foundation for a $1M head start.