It's a common misconception that retirement accounts are just for adults. The reality is, you can open a Roth IRA for a child, giving them an almost unbelievable head start on their financial future. This isn't just a souped-up savings account; it’s a genuine investment tool that allows a minor's earned money to grow and eventually be withdrawn in retirement, completely tax-free.

The Ultimate Gift: A Roth IRA for Kids

Think of it like this: you plant a small financial seed for your child today. Given decades of time to grow, that tiny seed can flourish into a massive tree. A Roth IRA takes that concept a step further—it ensures that every piece of fruit harvested from that tree, for their entire life, is theirs to keep, free from taxes. That’s the real magic of a Roth IRA for kids.

This is so much more powerful than a simple piggy bank. It's a foundational lesson in building long-term wealth, all powered by the incredible force of compound growth. When your child invests, their money earns returns. Pretty soon, those returns start earning their own returns, creating a snowball effect that can turn a few small contributions today into a massive nest egg 50 or 60 years from now.

The Financial Superpower of an Early Start

The single greatest asset a young investor has is time. An enormous amount of it.

To put it in perspective, a one-time contribution of $1,000 at age 10 could easily grow to over $45,000 by age 65, assuming a standard 8% average annual return—and that's without ever adding another dime. If that same person waited until age 30 to invest the same $1,000, they'd end up with less than $11,000. Time is the rocket fuel for a child’s investments.

Starting this early gives your child a financial edge that's almost impossible to replicate later in life. It provides them with:

- Decades of Tax-Free Growth: All the gains their investments make over the years grow completely untaxed.

- Tax-Free Retirement Withdrawals: Once they retire, every penny they pull out is theirs, with no income tax bill attached.

- A Crash Course in Financial Literacy: Actively funding and watching a Roth IRA grow is one of the best ways to teach a kid about earning, saving, and the power of investing.

What Counts as "Earned Income" for a Child?

There’s one non-negotiable rule to unlock this financial superpower: the child absolutely must have earned income. This is the key that opens the door. So, what does the IRS consider "earned"?

Simply put, earned income is money paid for real work the child has actually done. It can't be an allowance, a cash gift for good grades, or payment for routine household chores. The IRS looks for a legitimate connection between work performed and money received.

For instance, money from babysitting, mowing lawns, lifeguarding at the local pool, or even working a real job at a family-owned business all counts. It has to be a legitimate job with reasonable pay for the work performed. Getting this part right is crucial for compliance. Once you understand this rule, you can help your child find all sorts of creative ways to start earning and funding their own journey to financial freedom.

Getting the Rules Right for a Kid's Roth IRA

The idea of starting a Roth IRA for a child is incredibly powerful, but to unlock its full potential, you have to play by the IRS's rules. They aren't trying to trick you, but they are firm. Everything hinges on one non-negotiable requirement: earned income.

Without it, a child simply can't contribute to a Roth IRA. This is the key that starts the engine. The money has to come from real work your child has done—gifts and weekly allowances don't make the cut.

What Counts as Earned Income?

So, what does the IRS consider "earned income"? It's simply money paid for actual services. Think of it as compensation from a real job, whether that's a formal W-2 position or cash earned from a side hustle.

For most kids, this will look a lot like self-employment. Here are some classic examples that absolutely qualify:

- Babysitting for the family down the street.

- Mowing lawns or shoveling snow for neighbors.

- Tutoring younger kids.

- Working a summer job as a lifeguard or at the local ice cream shop.

- Helping out in a family business, as long as the work is legitimate and they're paid a reasonable wage for it.

What’s great is that this flexibility lets kids channel their first forays into work directly into their retirement savings. But it's equally important to know what doesn't count. Birthday cash from grandma, holiday money, or payments for doing their regular household chores won't work.

Document Everything: Your Proof of Income

When your child is their own boss, keeping good records is your most important job. You need to be ready to show the IRS that the income was real and the work actually happened. This paperwork is your proof.

Key Takeaway: You absolutely must keep a clear paper trail connecting your child's work to their earnings. Without it, the IRS could disqualify the contributions and you might face penalties.

Set up a simple system to track everything. A basic spreadsheet or even a dedicated notebook is all you need. For every job, make sure you log:

- The date the work was done.

- A quick description of the job (e.g., "Walked the Miller's dog").

- How much they were paid.

- The name and contact info of the person who paid them.

For bigger jobs, you could even have your child create a simple invoice. This isn't just about satisfying the IRS; it's a fantastic way to teach them real-world business skills from day one.

Sticking to the Contribution Limits

Once you have documented earned income, it's time to contribute. But there are limits. The rule is straightforward: you can contribute up to 100% of their total earned income for the year, but no more than the annual maximum the IRS allows.

For 2024, the maximum contribution is $7,000. So, your child can contribute whichever amount is less: their total earned income for the year or $7,000. If your teen earns $2,000 lifeguarding over the summer, their Roth IRA contribution for the year is capped at $2,000.

Remember, these contributions are made with after-tax dollars, so there’s no immediate tax deduction. The real magic happens later: all qualified withdrawals after age 59½ are completely tax-free, provided the account has been open for at least five years. Following these rules is how you can truly supercharge your child's retirement savings.

How to Open a Custodial Roth IRA Step by Step

Alright, let's get down to the brass tacks. Opening a Roth IRA for kids might sound intimidating, but it’s actually a pretty straightforward process once you break it down. This is the part where the rubber meets the road—where you move from theory to action and put your child on a real path to financial freedom. Think of yourself as the general contractor for your kid's financial future. You're about to lay a rock-solid foundation.

The first, and most critical, decision is picking the right financial institution. You can't just walk into any bank; you specifically need a brokerage firm that offers custodial Roth IRAs.

Step 1: Choose Your Brokerage

Not all brokerage firms are the same, especially when it comes to accounts for minors. You’re looking for a long-term partner here, so it really pays to be picky.

Here’s what I always tell parents to look for:

- Low Fees: Hunt for brokerages with no annual fees on their custodial accounts and a great selection of commission-free ETFs and mutual funds. Fees are like termites, slowly eating away at your returns. Over decades, minimizing them is a huge deal.

- Investment Options: A good firm will give you plenty of choices, from simple "set it and forget it" target-date funds to individual stocks. This flexibility allows the portfolio to get more sophisticated as your child's financial knowledge grows.

- User-Friendly Platform: Let's be honest, you're going to be the one managing this account for a while. An intuitive website and a good mobile app make contributing, investing, and checking in so much easier.

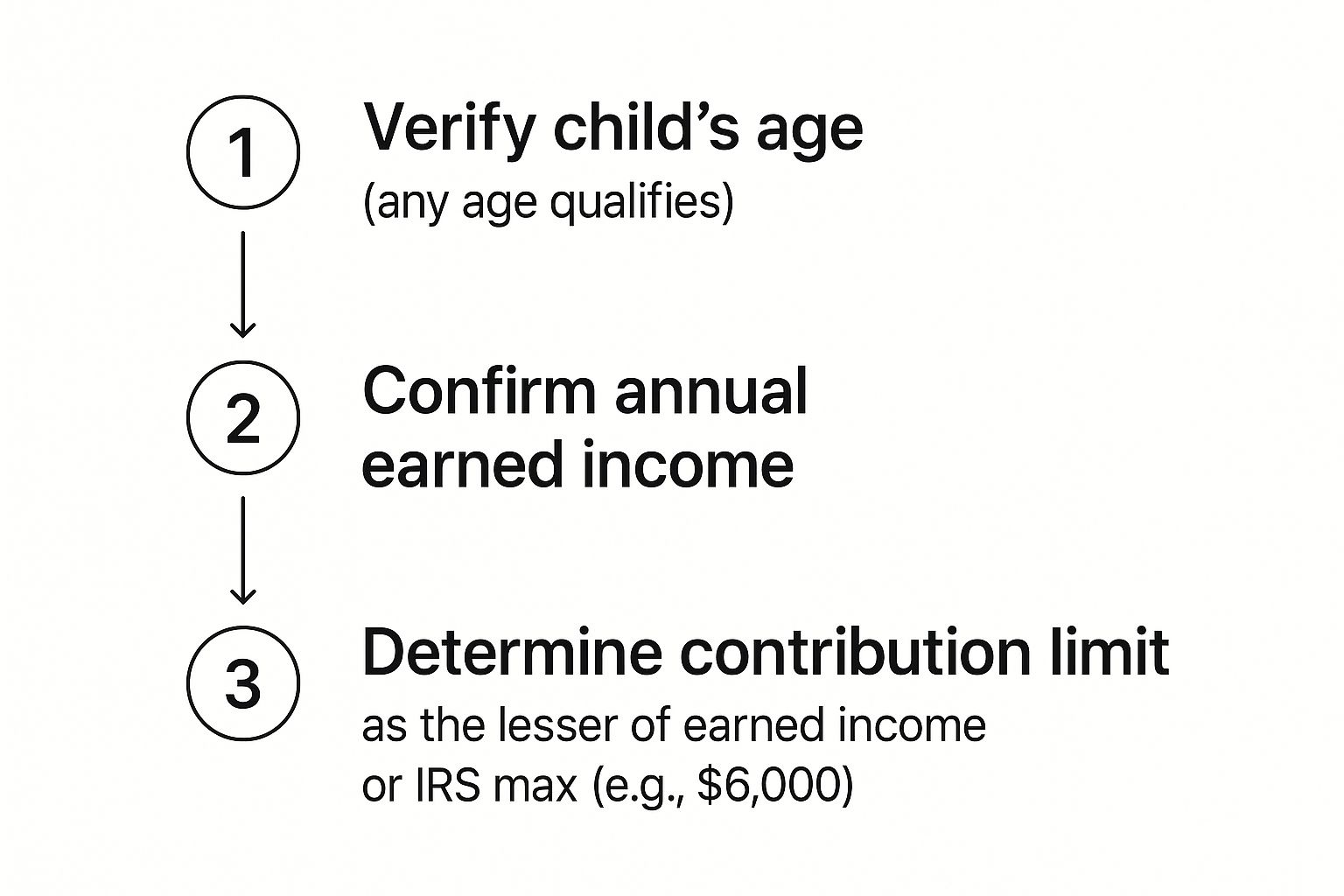

Before you even start an application, it’s worth a quick check to make sure everything lines up. This simple chart lays out the absolute must-haves.

As you can see, it all boils down to two things: the child must have legitimate earned income, and the contribution can't be more than what they earned (up to the annual IRS limit).

Step 2: Gather Your Documents

Once you’ve picked your brokerage, it’s time to get your paperwork in order. The firm needs to verify who you are and who your child is—this is a standard federal requirement to prevent fraud and protect everyone involved.

You'll almost certainly need:

- For the Custodian (You): Your basic info like name, address, DOB, and Social Security number. Have your driver's license or another government-issued ID handy, too.

- For the Minor (Your Child): Their full name, address, date of birth, and Social Security number.

Having these details ready beforehand makes the whole application process a breeze.

Step 3: Complete and Submit the Application

Now you're ready to fill out the form. Most of the big brokerages let you do this online in about 15 minutes. During this step, you'll officially name yourself as the "custodian" and your child as the "beneficiary." This simply means you have the legal authority to manage the account until they come of age in your state, which is usually 18 or 21.

If you want a deeper dive into the specifics, you can explore our detailed guide on what a custodial Roth IRA really means.

Pro Tip: Don't do this alone! Pull up a chair and have your child sit with you while you fill out the application. Point to their name on the screen and explain that they are the owner of the account. It makes the idea of saving and ownership feel real and exciting for them.

Step 4: Fund the Account

After you get the "approved!" email, it's time to put some money in. You’ll link your bank account to make a transfer. Just remember the golden rule: you can only contribute up to the amount of your child's earned income for the year, or the annual IRS maximum—whichever is less.

Step 5: Select the Investments

This is the fun part—putting that money to work. With decades to grow, a child's portfolio has a massive advantage. You can afford to be focused on long-term growth. To start, most parents keep it simple with low-cost, diversified options.

A couple of fantastic starting points are:

- Broad-Market Index Funds: Think of an S&P 500 fund. With one purchase, you own a tiny slice of 500 of America's biggest companies. It’s instant diversification.

- Target-Date Funds: These are designed to be hands-off. You pick a fund based on an estimated retirement year (say, 2065), and it automatically rebalances over time, becoming more conservative as it nears that date.

Follow these five steps, and you’ll have successfully opened a Roth IRA for your child. It's one of the most powerful financial gifts you can ever give them.

Smart Ways for Kids to Earn Income

To get a Roth IRA for kids up and running, you need one non-negotiable ingredient: earned income. Think of it as the fuel for their financial future. The idea of a child earning "real" money might seem tricky, but opportunities are everywhere once you start looking.

The crucial distinction here is between an allowance and actual wages. We're not talking about paying for routine household chores. We're talking about real work for real pay—the kind of income the IRS recognizes and the kind that can kickstart decades of compound growth.

The Parent-as-Employer Model

One of the cleanest and most direct ways to generate earned income for your child is to hire them in your own business. This isn't a loophole; it's a legitimate strategy, but you have to play by the rules. The IRS is perfectly fine with this, as long as the arrangement is legitimate.

Two rules are paramount:

- The job must be real. The work your child does must be genuinely necessary for your business operations.

- The pay must be reasonable. You have to pay them a fair market wage for the task. You can't pay your 10-year-old $100 an hour to shred paper. What would you pay a stranger to do the same job? That's your benchmark.

For example, you could legitimately hire your child for tasks like:

- Cleaning the office or organizing supplies.

- Filing, scanning, or handling simple data entry.

- Modeling for your business's website or social media photos.

- Stuffing envelopes or preparing mailers.

For a deeper dive into job ideas, check out our guide on how kids can earn money. By formalizing their employment with paychecks and maybe even a W-2, you not only satisfy the IRS but also give your child an invaluable first lesson in professional life.

Entrepreneurial Ventures for Teens and Tweens

As kids get older, their capacity to handle real responsibility skyrockets. This is the perfect time to nurture their inner entrepreneur. Forget odd jobs—we're talking about building tiny businesses that teach them about marketing, customer service, and pricing their own value.

Some powerful ideas for budding entrepreneurs include:

- Social Media Management: Many small businesses are desperate for help with their social media. A tech-savvy teen can easily manage content calendars and post updates for a monthly retainer.

- Tutoring: Is your kid a mathlete or a history buff? They can turn that knowledge into cash by tutoring younger students in the neighborhood or online.

- Digital Design: With user-friendly tools like Canva, a creative teen can design flyers, social media graphics, or simple logos for local businesses and community groups.

- Dog Walking & Pet Sitting: This classic for a reason. It's a fantastic way to earn consistent money while learning about responsibility and scheduling.

The Golden Rule: Document Everything

No matter what job your child does, meticulous record-keeping is your best friend. This is the proof that turns their hard work into legitimate, Roth-eligible income.

Keep a simple but detailed log. A spreadsheet is perfect. Track the date, the client (even if it's you!), the specific service performed, and the payment received. This simple habit is your ultimate defense if the IRS ever has questions.

To help you brainstorm, here is a table with a few age-appropriate business ideas and how to get them started on the right foot.

Kid-Friendly Earned Income Ideas

| Business Idea | Best For Ages | Getting Started Tips | Record-Keeping |

|---|---|---|---|

| Lawn Care & Yard Work | 12+ | Create simple flyers to distribute in the neighborhood. Invest in basic tools like gloves and rakes. | Log each address, date of service, and payment amount. Take before/after photos. |

| Babysitting | 13+ (with training) | Take a Red Cross babysitting course. Start with family friends to build references. | Keep a calendar with dates, hours worked, and family names. Note the rate per hour. |

| Tutoring | 14+ | Focus on a subject they excel in. Advertise at the local library or community center. | Create a simple invoice for each session. Track hours and subjects taught. |

| Pet Sitting / Dog Walking | 10+ | Start with neighbors you know well. Ask for testimonials to build credibility. | Use a notebook or app to track walk times, feeding schedules, and payments from each pet owner. |

Ultimately, finding a way for your child to earn income does more than just fund their Roth IRA. It instills a powerful work ethic and gives them firsthand experience with the connection between effort and reward—a lesson that will pay dividends for the rest of their lives.

Comparing a Roth IRA to Other Kids' Savings Accounts

Picking the right savings account for your child is a bit like choosing the right tool for a job. You wouldn't use a sledgehammer to hang a picture frame, right? A Roth IRA for kids is an incredible tool for one very specific, very distant job—retirement. But to build a truly solid financial foundation for your child, you need to see how it fits in with the other tools available.

Each account has its own set of rules, tax benefits, and flexibility. It’s not about finding the one "best" account, but about understanding which one is the best fit for a particular goal. In fact, a really smart strategy often involves using a few of them in tandem.

Roth IRA vs 529 College Savings Plan

This is the most common showdown people consider, and for good reason. Both a Roth IRA and a 529 plan pack a serious tax-advantaged punch. The real difference comes down to their intended purpose. A 529 is precision-engineered for education costs, whereas a Roth IRA is built for the long game of retirement.

- How Taxes Work: Both accounts let your money grow tax-free, which is fantastic. But the catch is in the withdrawals. With a 529, withdrawals are tax-free only if you use the money for qualified education expenses (think tuition, books, room and board). With a Roth IRA, qualified withdrawals in retirement are tax-free for any reason whatsoever.

- Flexibility: Here’s where the Roth IRA really pulls ahead. You can pull out your direct contributions from a Roth IRA at any age, for any reason, with no taxes or penalties. If you try to use 529 funds for anything other than education, you’ll get hit with income tax and a 10% penalty on the earnings.

- Getting Money In: Anyone can contribute to a 529 plan for your child, and the limits are very high. A Roth IRA, on the other hand, requires the child to have actual earned income in that year, and they can't contribute more than what they earned.

A good way to think about it is that a 529 plan is like a specialist's tool, perfectly designed for one task. The Roth IRA is more of a high-quality multi-tool—it has a primary purpose but offers a lot of flexibility for other situations.

Roth IRA vs UTMA or UGMA Custodial Accounts

Next up are the custodial accounts known as UTMAs (Uniform Transfers to Minors Act) and UGMAs (Uniform Gifts to Minors Act). These are straightforward accounts that let you invest on behalf of a child. But unlike a Roth, they are not retirement accounts.

The most significant difference boils down to two things: control and taxes. Once your child reaches the age of majority in your state (usually 18 or 21), a UTMA/UGMA account is theirs, lock, stock, and barrel. They get full, unrestricted control of the money to do with as they please—whether you approve of their plans or not.

A Roth IRA, in contrast, keeps its retirement-focused guardrails up. Even when the child takes control of the account, the money is still inside an IRA, and the rules naturally discourage cashing it out for a new car or a lavish vacation.

From a tax standpoint, UTMA/UGMA accounts are also a bit of a headache. The earnings and gains are taxed each year according to the "kiddie tax" rules, which can be a real pain. That’s a world away from the completely tax-free growth happening inside a Roth IRA.

Roth IRA vs a Standard Savings Account

Finally, there’s the good old-fashioned savings account. It's the simplest of the bunch and a fantastic first step for teaching kids the basics of putting money aside for a short-term goal, like a new video game or bicycle. But for long-term growth, it’s just not in the same league.

The interest you earn in a savings account is minimal—often less than 1% per year—and it’s taxed as ordinary income. A Roth IRA lets you invest that money in the stock market, where you have the potential for much higher returns over the long haul, all of which grow completely tax-free.

Because there's no age minimum for a Roth IRA—only an income requirement—even a young kid with a summer job can get started. The contribution limit for 2024 is $7,000 (or their total earnings for the year, whichever is less). The power of starting this early is staggering; a small yearly contribution from a young age can easily balloon into more than half a million dollars by retirement thanks to decades of tax-free compounding. You can dive deeper into these benefits in this guide about why your kid needs a Roth IRA from NerdWallet.

In the end, it all comes back to your goal. For retirement, the Roth IRA is the undisputed champion. For college, the 529 is tailor-made. For general savings with maximum flexibility (but minimal tax benefits), a UTMA/UGMA is a solid choice. A truly comprehensive financial plan for your child will likely use these tools together to prepare them for whatever life throws their way.

Answering Your Top Questions About Kids' Roth IRAs

Once you grasp the incredible power of a Roth IRA for kids, the practical questions usually start bubbling up. You see the potential, but now you need to know how it all works in the real world. Let's dive into those common "what if" scenarios to clear things up and give you the confidence to manage the account effectively.

Think of this as the FAQ section you read after you’ve built the furniture. Getting these details right ensures you're maximizing this amazing financial tool for your child.

Can a Parent Match Their Child's Contributions?

This is a fantastic question and one I hear all the time. While you can't "match" their contribution like a company 401(k), you can absolutely gift your child the money to put into their account.

Here’s the crucial rule: the total amount contributed for the year can't be more than what your child actually earned.

So, if your teenager earns $2,500 from a summer lifeguarding job but spends every penny, you can give them a $2,500 gift to put straight into their Roth IRA. The IRS doesn't care where the cash comes from, only that the contribution is backed by legitimate earned income. It's a powerful way to supercharge their savings without them having to sacrifice their own spending money.

What Happens When My Child Turns 18?

This is a major milestone. When your child reaches the age of majority in your state (usually 18 or 21), the custodial part of the account simply goes away. The account legally becomes their own individual Roth IRA, and you are no longer the custodian.

They get the keys to the car, so to speak. Your child will have full control—they can make their own investment choices, change beneficiaries, and take money out. This transition is the perfect time for a real conversation about financial responsibility and the long-term vision for this account.

Preparing them for this handoff is key, so they understand the incredible gift they've been given.

Can We Use a Kid's Roth IRA for College?

Yes, you can, but you need to be very careful. One of the best features of a Roth IRA is that you can withdraw the direct contributions (the principal) at any time, for any reason, completely tax-free and penalty-free. That includes college tuition.

The catch involves the earnings. If you withdraw the investment growth before age 59½, that money is usually hit with both income tax and a 10% penalty. There's a special exception for qualified higher education expenses that waives the 10% penalty, but you'll still owe income tax on the earnings. For this reason, many families find it's better to use a dedicated college savings vehicle like a 529 plan and let the Roth IRA continue its powerful, tax-free growth for retirement.

What Are the Best Investments for a Child's Roth IRA?

Time is the most powerful ingredient in investing, and your child has more of it than anyone. With a time horizon of 50+ years, you can afford to be aggressive and focus entirely on growth, ignoring the short-term bumps in the market.

For most parents, keeping it simple is the smartest strategy. Here are two fantastic, straightforward options:

- Broad-Market Index Funds: Think of an S&P 500 or a total stock market index fund. These low-cost funds give you instant diversification by owning a tiny piece of hundreds or even thousands of top U.S. companies.

- Target-Date Funds: These are the ultimate "set it and forget it" solution. You just pick a fund with a retirement date way out in the future (like a 2065 fund), and it automatically adjusts its mix of stocks and bonds over the decades.

The goal isn't to pick the perfect stock. It's to choose a low-cost, diversified investment and then let the magic of compound growth do its work for the next half-century.

Ready to give your child a massive head start on their financial future? RothIRA.kids has you covered with a free starter guide, handy calculators, and tons of kid-friendly income ideas to get the ball rolling on building generational wealth.

Disclaimer: The content provided in this article is for informational and educational purposes only. We are not a financial advisor and do not provide financial advice. The information presented is not intended to be a substitute for professional financial, legal, or tax advice. You should consult with a qualified professional before making any financial decisions.