In a world of one-click purchases and invisible digital transactions, teaching kids about money has gone from a "nice-to-have" skill to an absolute necessity. Think of early money lessons as giving your child a financial compass. It helps them navigate their future, build a secure foundation, and confidently sidestep the all-too-common debt traps that snare so many adults.

Why Financial Education for Kids Is So Urgent

Let's face it: money isn't what it used to be. Most of us grew up with physical cash—coins and bills we could hold in our hands. Today’s kids are growing up where money is often just an abstract number on a screen, a quick tap of a card, or an in-app purchase. When money feels invisible, it's incredibly easy to lose sight of its real value.

Teaching financial literacy is a lot like teaching a child how to swim. You wouldn't toss them into the ocean and hope for the best; you'd start in the shallow end, teaching them how to float and tread water first. Giving them money skills early on is the same idea—it prepares them to handle the complex financial currents they'll definitely face as they grow up.

The Growing Gap Between Access and Knowledge

The need for this education is more pressing than ever. Kids are interacting with financial products and services at surprisingly young ages, but they often don't have the know-how to use them wisely. The data paints a pretty clear picture of this disconnect.

A recent OECD report on financial literacy among 15-year-olds revealed some eye-opening stats. While over 60% have a bank account or payment card and nearly 90% have bought something online, a staggering 20% still lack basic financial knowledge. This gap is a problem. It means millions of teens are navigating the financial world without the core skills to make smart decisions, leaving them vulnerable to debt and poor financial habits. You can dig deeper into these findings in the full report on the role of financial literacy from the OECD.

The real goal isn't just for kids to know what money is. It's about them understanding what money does and how to make it work for them. Financial literacy turns kids from passive consumers into active, thoughtful managers of their own financial lives.

Building a Foundation for Lifelong Success

Teaching kids about money is so much more than just giving them a piggy bank and calling it a day. It’s about building a mindset that will stick with them for life. The habits they form in childhood around earning, saving, and spending wisely compound over time—just like interest in a savings account.

These early lessons help shape adults who are:

- More confident when making financial choices.

- Less likely to fall into the trap of high-interest debt.

- Better prepared to handle unexpected financial emergencies.

- More capable of setting and reaching big life goals, like buying a home or retiring comfortably.

When you start these conversations early, you're not just teaching about dollars and cents. You're giving them the tools for independence, responsibility, and security. You're building the foundation for a capable and resilient adult.

The Four Pillars of Money for Kids

Think of building a strong financial future for your kids like building a house. You can't just throw a roof on and hope for the best; you need to start with a solid foundation. When it comes to money, that foundation rests on four key pillars: Earning, Saving, Spending, and Giving.

Grasping these four ideas gives kids a simple but surprisingly powerful way to think about every dollar that ever comes their way. It takes money from being some big, confusing, abstract thing and turns it into a practical tool they can actually understand and manage.

Let's break down how to teach each one.

Earning: Connecting Work to Money

It all starts with Earning. This is where kids first connect the dots between effort and reward—the idea that money comes from working or providing something of value. It’s a game-changing realization that money doesn't just magically show up in a wallet.

For little kids, you can introduce this with something as simple as an allowance for chores that go above and beyond their normal family duties. It's not about "paying them" to help around the house; it's about drawing a clear line between extra work and extra money.

As they grow, the concept of earning can get more sophisticated:

- Elementary School: This is the perfect age for small-scale entrepreneurship. Think a classic lemonade stand, selling homemade crafts, or walking a trusted neighbor's dog.

- Middle School: You can start introducing the concept of an hourly wage by having them help with bigger, one-off projects like a weekend of yard work or babysitting.

- High School: When they're ready, support them in finding that first real part-time job. This is where they learn about schedules, paychecks, and being accountable to a boss.

The core lesson here is profound: money is something you create through your own actions.

Saving: Paying Your Future Self First

Once they've earned some cash, the next pillar is Saving. Honestly, this might be the most powerful financial habit you can ever teach someone. Saving is just setting money aside for a goal, but the best way to frame it is as paying your future self first.

This single idea is the ultimate weapon against the instant gratification monster that lives inside all of us. When you teach a kid to automatically save a piece of every dollar they get, you're building up their "delayed gratification" muscle. Suddenly, saving isn't a boring chore; it's an exciting plan for getting something they really want down the road.

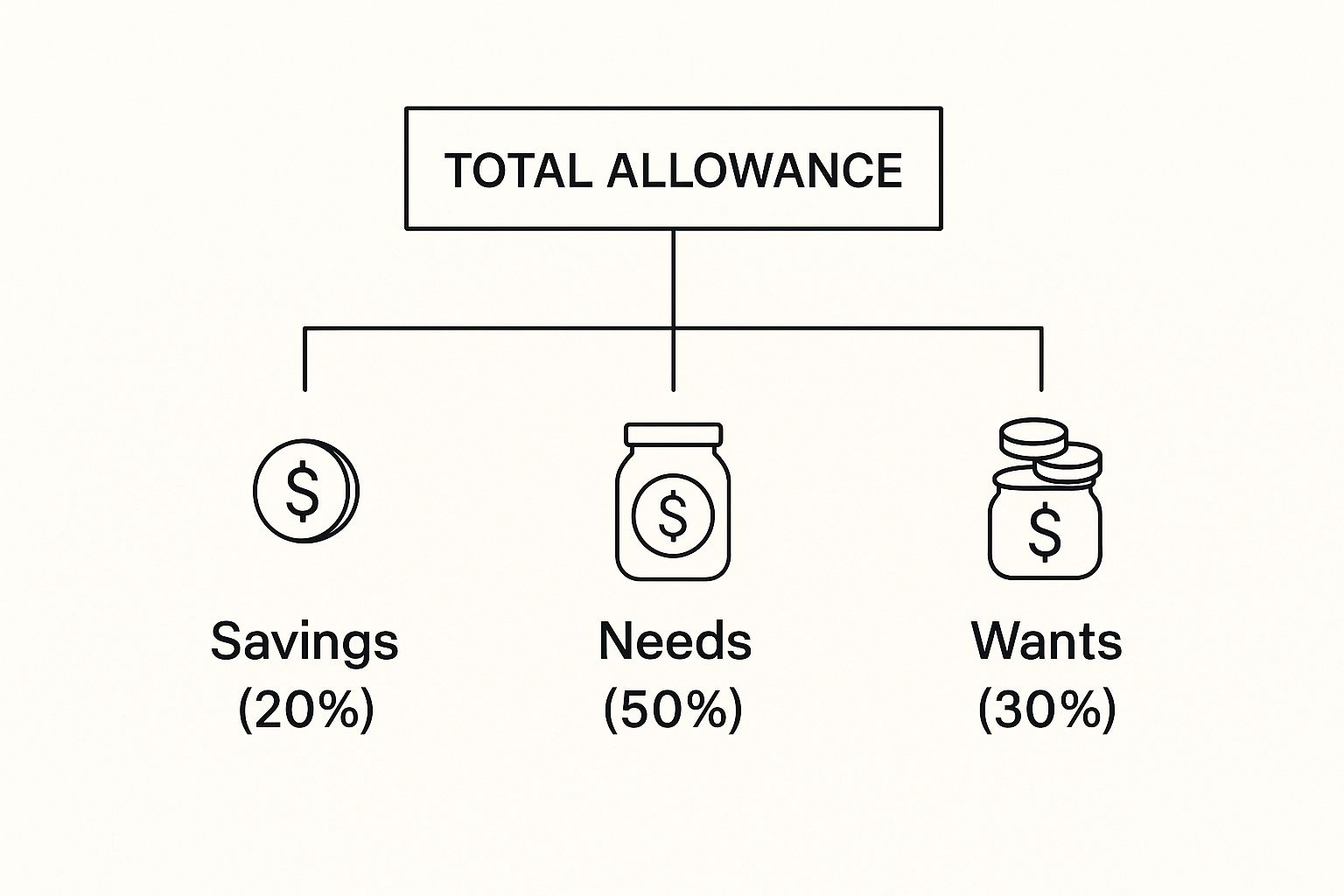

The infographic below shows a simple way to split up an allowance to make saving a priority.

This visual shows how even a small amount can be divided strategically, with a slice going straight to savings before there's even a chance to spend it.

Spending: Making Smart Choices

The third pillar, Spending, is where the rubber meets the road. Kids get to make actual decisions with their own money. The goal isn’t to stop them from spending—it’s to teach them how to do it wisely. The most important lesson here is understanding the difference between a need and a want.

A need is something you have to have to live, like food or a safe place to sleep. A want is something that’s just nice to have, like a new video game or trendy sneakers.

Helping a child truly get this difference is the key to responsible spending. You have to let them have control over their own money. The first time they blow their whole allowance on candy and then realize they don't have enough for the toy they've been eyeing, they learn a very real—and very memorable—lesson about opportunity cost. Choosing one thing means you can't have the other.

These little financial fumbles are priceless. They teach budgeting, setting priorities, and the real-world consequences of their choices in a safe, low-stakes environment.

Giving: Using Money to Do Good

The last pillar is Giving. This is what expands a child's financial perspective beyond just themselves. It shows them that money isn't only for buying things; it's also a powerful tool for making a positive impact on others.

Introducing the idea of charity early on builds empathy, gratitude, and a sense of responsibility to their community. It proves that their actions, no matter how small they seem, can truly help someone else.

Here are a few simple ways to encourage giving:

- Add a "Give" jar right next to their "Save" and "Spend" jars.

- Let them pick a charity or cause they genuinely care about to support.

- Involve them when your family gives back, whether it's buying a gift for a holiday toy drive or dropping off food at a local pantry.

By weaving these four pillars—Earning, Saving, Spending, and Giving—into your everyday family life, you give your kids a complete, well-rounded financial education. This framework gives them the tools and the mindset they need to build a life that is both financially secure and generous.

Hands-On Ways to Teach Money Skills

Let's be honest—talking about budgeting and saving can make a kid's eyes glaze over. These big, abstract ideas don't mean much until they can see them in action. The best way to make financial lessons stick is to get them out of your head and into their hands.

When children can physically see, touch, and manage their own money, the concepts suddenly click. It's all about turning everyday moments into powerful lessons that build real, lasting financial habits.

Start with Visual and Tangible Tools

For little kids, seeing is believing. Physical cash and clear containers are your best friends here because they make the fuzzy concept of "saving" totally concrete.

The classic three-jar system is a perfect example and works wonders. Just grab three clear jars and label them: Save, Spend, and Share. Anytime your child gets money, whether from an allowance or a birthday gift, you can help them split it up.

- Spend Jar: This is their "fun money" for small, right-now wants. It teaches them to work within a limit.

- Save Jar: This is for bigger goals, like that LEGO set or video game they’ve been eyeing. They can physically watch the money pile up, which makes saving feel exciting.

- Share Jar: This jar introduces the joy of giving, helping them understand that money can also be a tool to help others.

This simple setup offers a powerful visual. They can literally watch their savings grow, making the idea of waiting for something you really want feel much more satisfying.

Level Up to Real-World Financial Tools

As kids get older, they need to graduate from piggy banks to actual bank accounts. Introducing them to real financial tools is the natural next step, preparing them for the money decisions they’ll face as teens and young adults.

Helping them open their first bank account—usually a custodial or joint account you can oversee—is a huge milestone. Walk them through the whole process. Show them how to make a deposit, how to read a statement, and how to check their balance online. This makes the leap from physical cash to digital money feel way less intimidating.

Once the account is set up, you can introduce a simple budget. If they’re earning money from chores or a part-time job, sit down with them and map out a plan.

Budgeting Example for a Teen:

- Income: $50 per week from a part-time job.

- Savings Goal (20%): $10 goes straight into their savings account for a big goal, like a car.

- Necessary Spending: $15 for their share of the phone bill or gas money.

- Flexible Spending: $25 for going out with friends, buying snacks, or other personal wants.

This kind of hands-on practice teaches them how to prioritize and make smart choices with their own money. For a deeper dive, check out our guide on how to teach kids about money.

Involve Them in Family Finances

One of the most powerful things you can do is pull back the curtain on your own family's finances. When you include kids in age-appropriate money conversations, it makes the topic feel normal and approachable, not like some big, scary secret.

You don't need to show them your mortgage statement, but you can bring them into smaller, more understandable decisions. Planning a family vacation is a fantastic opportunity. Set a budget together and let them help research the cost of activities or meals. It’s a real-world lesson in planning and making trade-offs.

This kind of practical financial training is gaining traction worldwide. For example, Global Money Week 2025 in the Czech Republic attracted over 118,000 young participants, and its Financial Literacy Competition involved more than 88,000 students. Events like this show just how effective interactive learning can be, equipping the next generation with the skills to budget, invest, and stay out of debt.

By using these hands-on methods, you're not just teaching them about money; you're building a foundation of confidence that will set them up for a secure financial future.

How to Tackle Advanced Topics Like Investing and Credit

Once your kids have a handle on the basics of earning and saving, their financial world starts to open up. It’s time to introduce them to the more powerful concepts they’ll need to navigate the major money decisions of young adulthood, from student loans to their very first investments.

Topics like investing and credit can sound intimidating, but they don’t have to be. By breaking them down into simple, relatable ideas, you can give your teen the confidence to use these financial tools responsibly. The goal isn’t to make them a Wall Street wizard overnight. It’s about building a solid foundation for a lifetime of smart decisions.

Unlocking the Power of Compounding

If there's one "advanced" concept to teach, it's compounding interest. This is the engine that drives all long-term wealth. So, how do you explain it without pulling out a spreadsheet and watching their eyes glaze over?

Use the "snowball analogy." Picture a tiny snowball at the very top of a long, snowy hill. Give it a small push, and as it rolls, it starts picking up more snow. The bigger it gets, the more snow it collects with every single turn, making it grow faster and faster.

That’s exactly how your money works when it compounds.

- The initial snowball is your starting investment (the principal).

- The new snow it picks up is the interest or return it earns.

- The magic happens when that bigger snowball starts picking up even more snow on its next rotation. Your money is now earning returns on both the original amount and all the previous returns it has already gathered.

This is precisely why starting early is a game-changer. A small amount of money invested for a teen has decades to roll down that hill, growing into something far larger than a bigger sum invested later in life. Time is their single greatest financial advantage.

Introducing Low-Risk Investing

Once they grasp the why of compounding, you can show them the how. For teens just starting out, the best approach is to begin with low-risk investment options that are easy to understand. The goal is simply to get their money working for them without taking on big, scary risks.

A fantastic and practical starting point is a Roth IRA for kids. This is a special retirement account you can open for a minor as long as they have legitimate earned income. The money they put in is "after-tax," which means all the future growth and the money they pull out in retirement are completely tax-free.

Here’s why it’s such a powerful teaching tool:

- It’s a real-world application: They see money from their part-time job go into a real investment account with their name on it.

- It leverages time: A few thousand dollars invested as a teen can grow into a massive sum over 50+ years, all thanks to that compounding snowball.

- It teaches a vital lesson: It connects the act of working directly to building long-term wealth, not just to funding this weekend's fun.

To get into the specifics, check out this great guide on investing for minors that breaks down the whole process. A Roth IRA can transform a summer job into an incredible head start on a secure retirement.

Demystifying Credit and Debt

Finally, it’s absolutely critical to pull back the curtain on credit. Too many young adults first encounter credit through a student loan application or a tempting credit card offer during college, often without fully understanding the rules of the game.

Explain that credit is really just borrowing money that you promise to pay back. A good credit score is like a financial report card; it shows lenders that you’re a trustworthy and responsible borrower. A high score makes it much easier and cheaper to borrow for big things later on, like a car or a house.

On the flip side, debt is the reality of what you owe. It’s essential to be upfront about the dangers of high-interest debt, especially from credit cards.

Credit Card Debt Example

Imagine your teen buys a $500 video game console with a credit card that has a 20% interest rate. If they only make the minimum payment each month (let's say $25), it would take them more than two years to pay it off, and they'd end up paying nearly $100 in interest alone. That’s $100 for nothing!

Teaching them to view credit as a useful tool—not a blank check—is one of the most important lessons you can offer. It prepares them to sidestep common financial traps and build a strong, positive financial reputation right from the start.

Common Questions About Teaching Kids Money

Starting to teach your kids about money is a huge step, and it's completely normal to have questions. In fact, it’s one of the most important things you’ll ever teach them. Knowing how to handle the tricky parts gives you the confidence to turn everyday moments into powerful lessons.

Let’s walk through some of the most common questions and concerns parents have. My goal here is to give you practical, straightforward advice you can start using right away to help your kids become financially savvy.

At What Age Should I Start Teaching My Child About Money?

It’s never too early to start. You can begin introducing simple money concepts as soon as your child can count, usually around age three or four. Research actually shows that kids who get a head start on financial education by age seven tend to build much healthier money habits as they grow up.

At this stage, it's all about making money tangible. We're talking about introducing coins, explaining that we use them to buy things at the store, and maybe getting a clear piggy bank. Seeing the coins pile up makes the idea of saving real and exciting. The trick is to keep it simple and build on these ideas as your child gets older.

Should I Pay My Kids for Chores or Give an Allowance?

This is the classic debate, and honestly, there's no single right answer—it comes down to what works for your family. That said, many experts I've talked to recommend keeping basic chores separate from a regular allowance. Why? Because it teaches two different, but equally critical, life lessons.

Think of an allowance as a tool for learning, not a wage. It's a consistent, predictable amount of money they can use to practice budgeting, saving, and spending. Then, you can offer to pay them for "extra" jobs that fall outside their normal family responsibilities, like washing the car or a big yard cleanup project.

This two-pronged approach accomplishes a couple of things:

- A regular allowance gives them a reliable "paycheck" to practice managing.

- Paying for extra work creates a direct link between putting in more effort and earning more money.

What Are the Best Tools to Help Teach Financial Literacy?

Having the right tools can make all the difference, turning abstract ideas into something kids can actually grasp. For the little ones, physical and visual aids are your best friends.

The classic three-jar system—one for Saving, one for Spending, and one for Giving—is a fantastic starting point. It physically sorts their money by its purpose, making a complex financial idea simple enough for a child to see and understand.

As they get older, you can level up the toolkit:

- Custodial Bank Accounts: Opening their first real bank account is a rite of passage. It introduces them to the basics of deposits, withdrawals, and maybe even understanding a bank statement.

- Debit Cards for Kids: Several great services now offer debit cards specifically for kids, complete with apps. These allow you to set spending limits, assign chores, and track their savings goals together.

- Educational Games: Don't underestimate the power of play! Board games like Monopoly or The Game of Life are amazing for simulating real-world money decisions in a fun, low-risk way.

How Do I Teach My Child About Digital Money and Safety?

In a world of tapping cards and one-click checkouts, it's more important than ever to show kids that digital money is real money. It's not just a number on a screen.

A simple way to do this is to involve them. The next time you pay with your card or a phone app, pull up your bank statement later and show them the transaction. This connects the invisible act of paying with a real-world financial result.

It’s also the perfect time to talk about online safety—things like using strong passwords and why they should never share financial info online. If your teen has their own debit card, make a habit of reviewing their spending with them. It helps them see their own digital "footprint" and builds the responsible habits they'll need for life.

Here is the rewritten section, designed to sound like it was written by an experienced human expert.

Your Part in Raising a Financially Savvy Generation

As a parent, you wear a lot of hats, but one of your most important roles is being your child's first money coach. Teaching kids financial literacy isn't about sitting them down for a formal lecture. It's an ongoing conversation that you weave into everyday life.

Think about it: a trip to the grocery store becomes a lesson in budgeting. A summer job isn't just about a paycheck; it’s a chance to see compounding interest work in real-time.

Why Your Involvement Matters Most

Your active participation is what makes these lessons stick. When you start talking about money early and connect it to real-world experiences, you're giving them the tools they'll use for the rest of their lives.

Every chat about needs versus wants, every dollar dropped into a savings jar, and every bit of income earned and invested builds a rock-solid foundation. You’re not just teaching them about dollars and cents; you're shaping their habits around responsibility, planning, and self-confidence.

The time you put in now is a direct investment in their future. You're helping raise a generation of adults who feel empowered by their finances, not intimidated by them—ready for whatever comes their way.

Ultimately, you're their most trusted guide on this journey. By making money an open, normal topic of conversation, you're giving your kids a huge head start. The small, consistent lessons you teach today will compound over the years, paving the way for a secure and prosperous future.

Ready to give your child an incredible head start on their financial future? Explore how RothIRA.kids can help you turn their early income into a powerful engine for generational wealth. Visit https://rothira.kids to learn more.

Disclaimer: The information provided in this article is for educational and informational purposes only and does not constitute financial advice. We are not financial advisors. All financial decisions should be made with the guidance of a qualified professional.