When it comes to investing for a child's future, the single best piece of advice is to start now. It might sound cliché, but time truly is your greatest superpower. Even small, regular contributions can blossom into a life-changing sum when given enough years to grow. Think of it as planting a tree—the sooner you get that sapling in the ground, the more time it has to mature into something strong and substantial.

Why Starting Early Is Your Greatest Advantage

Every dollar you invest for a child today has decades ahead of it to work, grow, and multiply. This isn't just about stashing away cash; it's about building a financial foundation that can support them through some of life's biggest moments.

The money you set aside now can make a huge difference down the road, covering expenses that can define a young adult's future. These goals often include:

- Higher Education: Helping them afford college or trade school without being saddled with mountains of student debt.

- A First Home: Providing a solid down payment that turns the dream of homeownership into a tangible reality.

- Starting a Business: Giving them the seed money to chase an entrepreneurial dream.

- A Safety Net: Creating a financial cushion that empowers them to take smart risks, travel, or handle unexpected curveballs with confidence.

The Power of a Head Start in Numbers

Let's put this into perspective. The magic ingredient here is compound interest, where your investment earnings start generating their own earnings. The more time you have, the more powerful this effect becomes.

An investment started at birth has an 18-year head start on one started when they graduate high school. That's nearly two decades of potential growth you simply can't get back.

To see just how dramatic the difference is, look at this simple scenario.

Impact of Starting Age on a Child's Investment

| Starting Age | Investment Value at Age 18 | Investment Value at Age 25 | Total Contribution |

|---|---|---|---|

| Birth | $46,260 | $91,524 | $30,000 |

| Age 5 | $27,030 | $56,766 | $24,000 |

| Age 10 | $12,335 | $30,865 | $18,000 |

| Age 15 | $3,908 | $13,296 | $12,000 |

As you can see, starting at birth with the same monthly contribution results in nearly $40,000 more at age 25 compared to waiting until the child is 10. The earlier start required only $12,000 more in total contributions but generated significantly more wealth, all thanks to time.

Unlocking a Future of Possibilities

Ultimately, investing for your child is about giving them the gift of choice. It's about empowering them to make decisions based on their passions and ambitions, not just their financial constraints.

By taking action now, you're not just saving money; you're building a legacy of security and opportunity that will shape their entire life. Whether you're just starting to explore your options or looking for better strategies, learning about investing for minors is the first critical step toward that goal.

Understanding the Magic of Compound Growth

When you begin investing for a child's future, you're tapping into a force so powerful it's been called the "eighth wonder of the world." That force is compound growth, and it's the real secret sauce that will fuel your child’s financial well-being for decades to come.

At its heart, compounding is a simple concept. It's the process where your investment earns a return, and then that return starts earning its own return. This feedback loop creates a cycle of accelerating growth that gets more and more potent every single year.

The Snowball Effect Explained

Think of your first investment as a small snowball at the top of a very long, snowy hill. When you give it that first push, it starts rolling. As it travels, it doesn't just stay the same size—it picks up more snow, getting bigger and heavier with every rotation.

The bigger the snowball gets, the more snow it collects, and the faster it accelerates. That’s exactly what compounding does for your child’s money. Your contributions are the small snowball, and the market returns are the fresh snow it gathers along the way. Given enough time, that little snowball can grow into an enormous boulder of wealth.

This principle is about more than just money. Research consistently shows that small, early advantages often lead to massive long-term gains in other areas of life, too.

"The positive long-term effects of early learning interventions are among the strongest in economics. Researchers have found that students attending Tulsa’s universal pre-K exhibit better language and math skills through elementary school, and better executive function."

Just as early education lays a foundation for a lifetime of learning, early investing builds the foundation for financial security. The most important ingredient is giving that snowball as much time as possible to roll and grow.

Compounding in Action: A Tale of Two Timelines

To truly grasp the power of starting early, let's look at a real-world example. We'll use a modest monthly investment of $100. The difference in the final amount over one, two, and three decades is staggering, and it's all thanks to the power of compounding.

Example: The Growth of $100 Per Month

Let's assume a hypothetical 7% average annual return, which is a common historical benchmark for the stock market.

-

After 10 Years:

- You've contributed a total of $12,000.

- Your account would grow to about $17,300.

- The growth from compounding is $5,300.

-

After 20 Years:

- You've contributed a total of $24,000.

- Your investment would jump to roughly $52,000.

- The growth is now a whopping $28,000—more than you put in!

-

After 30 Years:

- You've contributed a total of $36,000.

- Your investment could reach an incredible $122,000.

- The growth from compounding is nearly $86,000.

The numbers make it crystal clear: the truly explosive growth happens in the later years. In the first decade, your contributions do most of the work. But by the third decade, your money's earnings are working far harder than you are, creating a powerful wealth-building machine for your child. Every year you delay is a year of that incredible exponential growth you can never get back.

Choosing the Right Investment Account for Your Family

Once you get your head around the incredible power of compound interest, the next logical question is: "Okay, so where do I actually put the money?" That's a great question, because not all investment accounts are built the same.

Think of them like different tools in a toolbox. Each one has a unique purpose, its own set of rules, and specific tax benefits designed for different long-term goals. The three heavy hitters you’ll hear about most are 529 Plans, Custodial Accounts (UGMA/UTMA), and Custodial Roth IRAs. Figuring out which one is right for your family really boils down to what you want the money to achieve—paying for college, giving them a flexible nest egg, or launching their retirement savings light-years ahead of schedule.

The Education-Focused Powerhouse: 529 Plans

If your number one goal is saving for college, the 529 Plan is tough to beat. It's purpose-built for education savings, offering some fantastic tax advantages that make it a go-to for many parents.

So, how does it work? The big win here is the tax treatment. Your money grows tax-deferred, meaning you don't pay taxes on the gains year after year. Then, when it's time to pay for school, withdrawals are completely tax-free as long as you use them for qualified expenses. We're talking tuition, fees, room and board, books—even up to $10,000 in student loan repayments. Plus, many states sweeten the deal by offering a state income tax deduction on your contributions.

A critical feature is that you, the parent or guardian, stay in the driver's seat. The child is the beneficiary, but they can't just dip into the funds themselves. This ensures the money is used for its intended purpose. And if your child decides college isn't their path? No problem. You can simply change the beneficiary to another eligible family member, including yourself.

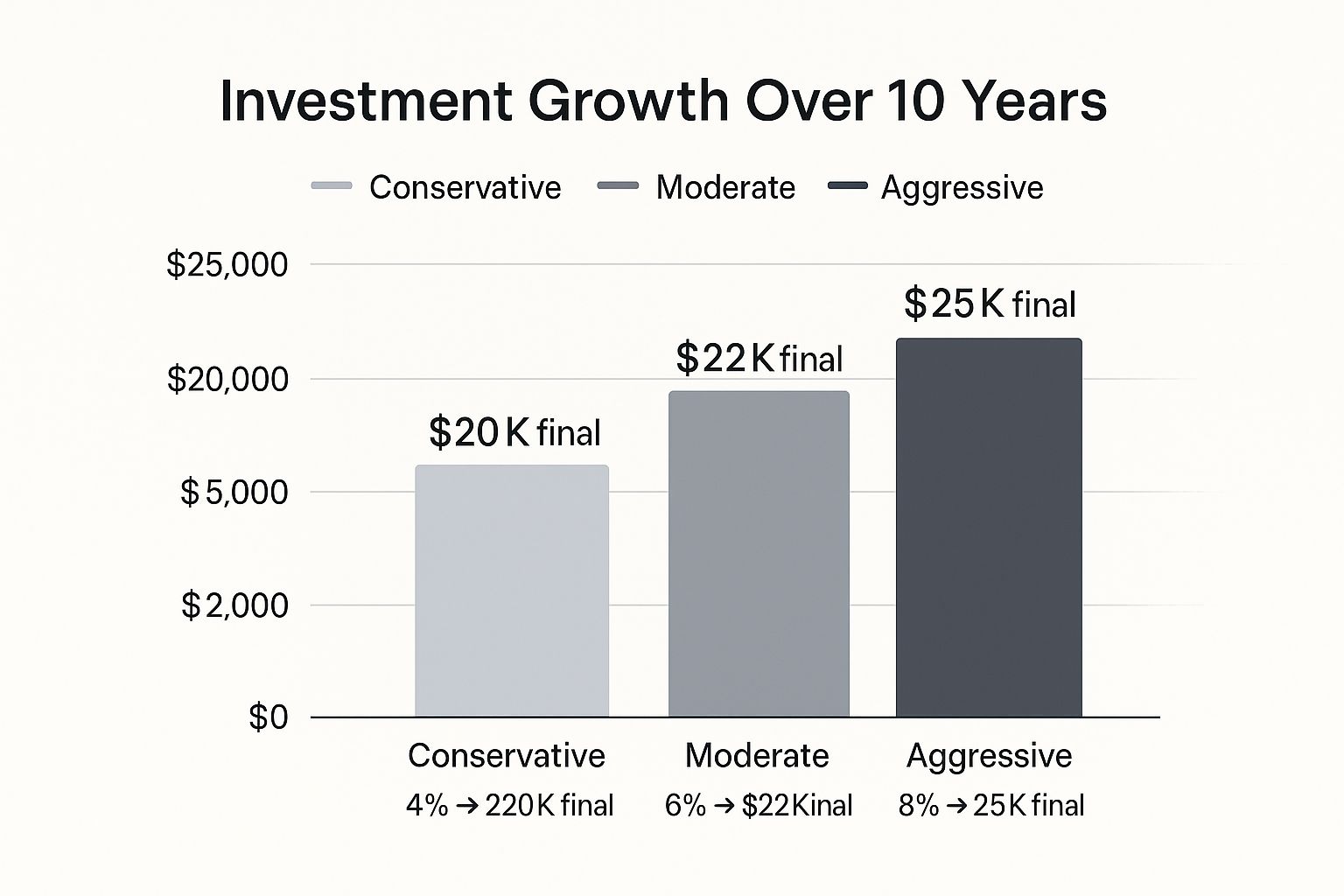

This chart really drives home how much your investment choices matter inside a 529.

As you can see, shifting from a conservative to a more aggressive strategy can mean a difference of thousands of dollars over the long haul. It's a powerful reminder that how you invest within the account is just as important as starting early.

The Flexible All-Rounder: Custodial Accounts (UGMA/UTMA)

But what if you want to give your child a financial head start that isn't tied strictly to education? That's where a Custodial Account shines. These accounts, governed by either the Uniform Gifts to Minors Act (UGMA) or the Uniform Transfers to Minors Act (UTMA), are all about flexibility.

Unlike a 529, the money in a custodial account can be used for anything that benefits the child. It could be their first car, a down payment on a home, or even seed money to start a business. The funds are legally an irrevocable gift to the child. The one major catch? When your child reaches the age of majority (usually 18 or 21, depending on your state), they get full, unrestricted control of the account. This is both its greatest strength and something to seriously consider—you have to be comfortable with your child managing what could be a large sum of money as a young adult.

From a tax perspective, a portion of the investment earnings can be taxed at the child's lower tax rate (often called the "kiddie tax"), but the rules can get a bit tricky, so it's something to be aware of.

The Long-Term Wealth Builder: Custodial Roth IRAs

Now for a truly powerful, and often overlooked, strategy for building generational wealth: the Custodial Roth IRA. This account lets a minor start saving for retirement decades earlier than most people even think about it, all while enjoying the incredible tax benefits of a Roth IRA.

Here’s the catch: the child must have legitimate earned income to be eligible to contribute. Mowing lawns, babysitting, a part-time job—it all counts. You contribute with after-tax dollars, but then the magic happens: the money grows completely tax-free, and every penny withdrawn in retirement is also tax-free. Given the ridiculously long time horizon for a child, the compounding effect in a tax-free environment is simply extraordinary.

As an added bonus, the contributions (but not the earnings) can be pulled out tax-free and penalty-free at any time, for any reason. This adds a nice layer of flexibility if they need the cash for a major life event, like buying their first home.

This focus on setting children up for success is a global priority. We see it in the work of organizations like The Global Partnership for Education (GPE), which has shown just how profound investing in kids' futures can be. Between 2021 and 2025, their initiatives helped 372 million children get better educational support, resulting in nearly 10 million more kids enrolling in school and the construction of almost 92,000 classrooms. You can read more about these impressive educational achievements and their ripple effect across communities worldwide.

Comparison of Child Investment Accounts

Choosing between these accounts can feel overwhelming, so I've put together a simple table to help you compare the key features side-by-side. Think about your main goal, and then see which account's features align best with it.

| Feature | 529 Plan | Custodial Account (UGMA/UTMA) | Custodial Roth IRA |

|---|---|---|---|

| Primary Goal | Education Savings | General Savings & Gifting | Retirement Savings |

| Contribution Source | Anyone can contribute | Anyone can contribute | Minor must have earned income |

| Tax on Growth | Tax-deferred | Taxable (potential "kiddie tax") | Tax-free |

| Tax on Withdrawals | Tax-free for qualified education | Taxable as capital gains | Tax-free in retirement |

| Use of Funds | Education-related expenses | Anything that benefits the child | Anything (contributions); retirement (earnings) |

| Account Control | Adult owner maintains control | Transfers to child at age 18/21 | Transfers to child at age 18/21 |

Ultimately, there's no single "best" account—only the one that's best for your family's specific circumstances and goals. You might even find that a combination of accounts makes the most sense. The key is to start somewhere.

How to Open Your Child's Investment Account

Alright, you've decided to start investing for a child's future. Fantastic. Moving from the idea of investing to actually doing it is where most people get stuck, but it’s far simpler than you might imagine. Once you’ve picked the right vehicle—whether it's a 529, a custodial account, or a Roth IRA—the next part is just paperwork.

The great news is that you're not navigating some complex financial maze. Most major firms have streamlined the process of opening accounts for minors, and you can usually get it done online from your couch.

Let’s walk through the exact steps you'll take.

Choosing Your Financial Institution

First things first: where will this account live? You'll need to pick a brokerage or financial institution. You’ve got plenty of great options, from legacy investment giants like Fidelity, Charles Schwab, and Vanguard to modern fintech apps designed specifically for families.

Here’s what I’d look for when making a choice:

- Account Availability: Does the firm actually offer the specific account you want? Not every brokerage offers a Custodial Roth IRA, for example, so double-check before you start.

- Investment Options: You want a wide menu of low-cost options. Think index funds and exchange-traded funds (ETFs)—these are the workhorses of long-term investing.

- Fees and Minimums: Keep an eye out for account maintenance fees or minimums to get started. Thankfully, many of the best brokerages now offer $0 account fees and no investment minimums.

- User Experience: Is the website a nightmare to navigate? A clean, simple platform makes managing the account feel less like a chore.

A bit of practical advice: The best platform is often the one you already know and trust. If you have a 401(k) or a personal brokerage account, see if they offer kids' accounts. Keeping things under one roof can make your financial life a whole lot easier.

Gathering Your Essential Documents

Once you’ve chosen a provider, the next step is to get your paperwork in order. I promise, doing this upfront makes the actual application process feel effortless. Think of it like organizing your ingredients before you start cooking—it just makes everything go smoother.

For both you (the custodian) and your child (the minor), you'll almost always need:

- Full Legal Name and Date of Birth

- Permanent Address

- Social Security Number (SSN) or Taxpayer Identification Number (TIN)

A quick but important note: The child's Social Security number is non-negotiable for opening any U.S. investment account in their name. If they don't have one yet, you can easily apply for one through the Social Security Administration.

For a Custodial Roth IRA, you have one extra piece of homework: you'll need proof of the child's earned income. This is a critical IRS requirement. For a complete rundown on this, you can learn more about how to start a Roth IRA for a child to make sure you're ticking all the right boxes from day one.

Navigating the Application and First Deposit

With your documents ready, the online application itself is usually a breeze—we’re talking less than 15 minutes. You'll plug in your info, your child's info, select the account type, and click "I agree" on the terms.

After the account is approved, it’s time for the final, most exciting step: funding it. Simply link your bank account to make the first deposit. And remember, you don't need a fortune to get started. The goal is just to begin. Even $25 or $50 is a perfect starting point.

Here's a pro-tip: Set up automatic, recurring deposits. It's the best way to invest consistently without having to actively think about it each month.

Once the money lands in the account, you have one last, crucial task: invest it. Cash just sitting there won't do much. You need to buy the actual investments—like a low-cost S&P 500 index fund—to put that money to work. With that one simple action, your child's investing journey has officially begun.

Common Investing Mistakes Parents Should Avoid

When you're investing for your child's future, building wealth is as much about dodging the landmines as it is about picking the right path. Getting this right means you need to sidestep a few common errors that can unfortunately cost you a lot of money and opportunity down the road.

Let's walk through the most frequent mistakes I see parents make and, more importantly, how you can steer clear of them.

The biggest mistake of all? Simply waiting to get started. It's so easy to fall into the trap of thinking, "I'll start when I have more money," or "I'll get to it when life isn't so chaotic." But as we've already covered, time is your single greatest ally in investing. Every year you put it off is a year of compound growth you can never get back. The perfect time to begin is right now, even if you're starting small.

Playing It Too Safe

Another classic misstep is being overly conservative with your investments. It might feel like the responsible thing to do—protecting your child's nest egg at all costs—but sticking to "safe" options like savings accounts or CDs can be a huge mistake over the long haul.

Think about it: your child has decades before they'll actually need this money. Their portfolio has plenty of time to ride out the market's natural ups and downs. The real danger here isn't a temporary market dip; it's inflation, which silently eats away at the value of your money. A portfolio that doesn't grow faster than inflation is actually losing purchasing power year after year. For a long-term goal like this, low-cost index funds or ETFs usually offer the right mix of risk and growth potential.

Overlooking the Tax Implications

You absolutely have to get a handle on the tax rules for whatever account you choose. It's a detail many parents miss, and it can make a big difference. For instance, are you familiar with the "kiddie tax"? This rule can apply to the investment earnings in a custodial account (an UGMA or UTMA) once they go over a certain amount.

Essentially, the kiddie tax means your child's investment income gets taxed at your higher parental tax rate, which can take a real bite out of your returns. This is exactly why tax-advantaged accounts like a 529 plan or a Custodial Roth IRA are often so attractive. Paying attention to these tax details from the get-go helps ensure more of the money you're saving actually ends up in your child's pocket.

The most effective investment strategies aren't just about picking winners. They're about systematically avoiding the big mistakes. A well-informed parent who sidesteps common blunders like delaying their start or ignoring tax rules often builds more wealth than a speculator chasing high returns.

The conversation around investing in our children's future is happening on a global scale, too, particularly when it comes to education. Nearly a quarter of a billion children worldwide need urgent help to access quality education, highlighting a critical need for sustained support. This global focus is a key reason the education market is projected to reach nearly $10 trillion by 2030, with early childhood being a major driver of that growth. You can dive deeper into these global education outlook findings on holoniq.com.

Ignoring the Power of Automation

The final trap many parents fall into is trying to "time the market" or making investment decisions based on emotion. It’s a classic story: they invest a lump sum when the market feels excitingly high or panic-sell when the headlines turn scary. A far better—and much less stressful—approach is to put the whole process on autopilot.

Here’s a simple checklist to automate your child's investing and take the emotion out of it:

- Set up recurring contributions: Schedule an automatic transfer from your bank to the investment account every month or with every paycheck. Set it and forget it.

- Automate your investments: Most brokerages let you set up automatic purchases of your chosen funds (like an S&P 500 index fund). This is the essence of dollar-cost averaging.

- Revisit annually, not daily: Check in on the account once a year to make sure things are on track, but please, resist the urge to react to the daily noise of the market.

By avoiding these common mistakes, you're not just investing money; you're building a smarter, more resilient financial foundation for your child's journey ahead.

Frequently Asked Questions About Child Investing

Diving into the world of investing for a child's future is exciting, but it almost always brings up a few practical questions. Once you’re ready to get started, you might start wondering about the day-to-day details and what-if scenarios. Here are some straightforward answers to the questions we hear most often from parents just like you.

Can Grandparents or Other Relatives Contribute to My Child's Account?

Absolutely! It’s a fantastic way for the whole family to support your child’s future. How they contribute just depends on the account you've set up.

-

For 529 plans: Anyone can contribute directly. In fact, many state-run 529 plans offer special gift-giving links you can share with family. This makes it incredibly easy for grandparents, aunts, and uncles to chip in for a birthday or holiday.

-

For custodial accounts (UGMA/UTMA): Gifting is just as simple. Friends and family can give money directly to the account, turning a traditional cash gift into a powerful, long-term investment.

This feature really turns saving into a community effort, letting everyone who cares about your child play a part in building their financial security.

How Much Should I Actually Invest for My Child?

There's no magic number here—the right amount is completely personal. It all comes down to what works for your family's budget, goals, and overall financial picture. Please don't let the pressure of finding the "perfect" amount stop you from getting started.

The most important step you can take is simply to start. Consistency over the long term is far more powerful than the size of your initial investment.

Even a small, regular contribution like $25 or $50 a month can blossom into a substantial nest egg over 10 or 20 years, all thanks to compounding. You can always adjust the amount and contribute more later on as your income grows or your circumstances change.

What Happens to a 529 Plan if My Child Does Not Go to College?

This is a very common worry, but the good news is you have options. The money is never lost, and these plans are more flexible than you might think.

Your first and best option is to simply change the beneficiary to another eligible family member. This could be another one of your kids, a grandchild, a niece or nephew, or even yourself if you decide to pursue further education. This transfer is completely penalty-free.

If that doesn't work, you can always withdraw the funds for non-qualified expenses. In this case, you'd owe regular income tax and a 10% federal penalty, but only on the earnings portion of the withdrawal. It’s not the ideal outcome, but it’s a solid backstop that ensures you can always get your money back if plans change.

Ready to give your child a decades-long head start on building wealth? At RothIRA.kids, we provide the tools and guidance to help you open a Roth IRA for your child, turning their early entrepreneurial efforts into a powerful, tax-free investment vehicle. Explore our free guides, calculators, and kid-friendly business ideas today at https://rothira.kids.

Disclaimer: The information provided in this article is for educational and informational purposes only and should not be construed as financial or investment advice. We are not financial advisors, and the content presented here is not a substitute for consultation with a qualified professional. Investment decisions should be based on your individual financial needs, objectives, and risk tolerance. We strongly recommend that you seek the advice of a certified financial planner or other qualified professional before making any investment decisions.