Earning money as a kid doesn't have to be complicated. Forget the lemonade stand for a second (though it's a classic for a reason!). We're talking about finding something you genuinely enjoy and turning it into your first real paying gig. This is where you start building skills, confidence, and a little bit of a bankroll.

Your First Steps To Earning Real Money

Landing that first paid job is a rite of passage. It's your first real taste of financial independence and a powerful lesson in the value of your work. Let's move beyond the basics and explore some genuine opportunities that align with what you're actually good at and interested in. This isn't just about chores; it's about finding an empowering way to make your own money.

The world of work for young people is wider than you might think. In fact, surveys show that over 50% of American teenagers hold some kind of part-time job by the time they're 16. Their annual earnings can range anywhere from $300 to $2,000. That kind of experience is priceless when it comes to learning about money. For a broader perspective, you can dive into some fascinating global youth employment trends to see the big picture.

Finding Your Niche

Okay, so where do you start? The most important first step is to look inward. What are you good at? What do you actually like doing? Don't just jump on the bandwagon because your friend is doing it. Your unique talents are your biggest asset.

Think about it:

- Love animals? Pet-sitting and dog-walking are always in demand.

- Prefer being outdoors? Seasonal yard work like mowing lawns, raking leaves, or shoveling snow can be surprisingly lucrative.

- Got a creative spark? With a parent's help, you could sell handmade crafts, jewelry, or even digital art online.

- A whiz with gadgets? Lots of adults would gladly pay for help with simple tech tasks, like setting up a new smartphone or organizing digital photos.

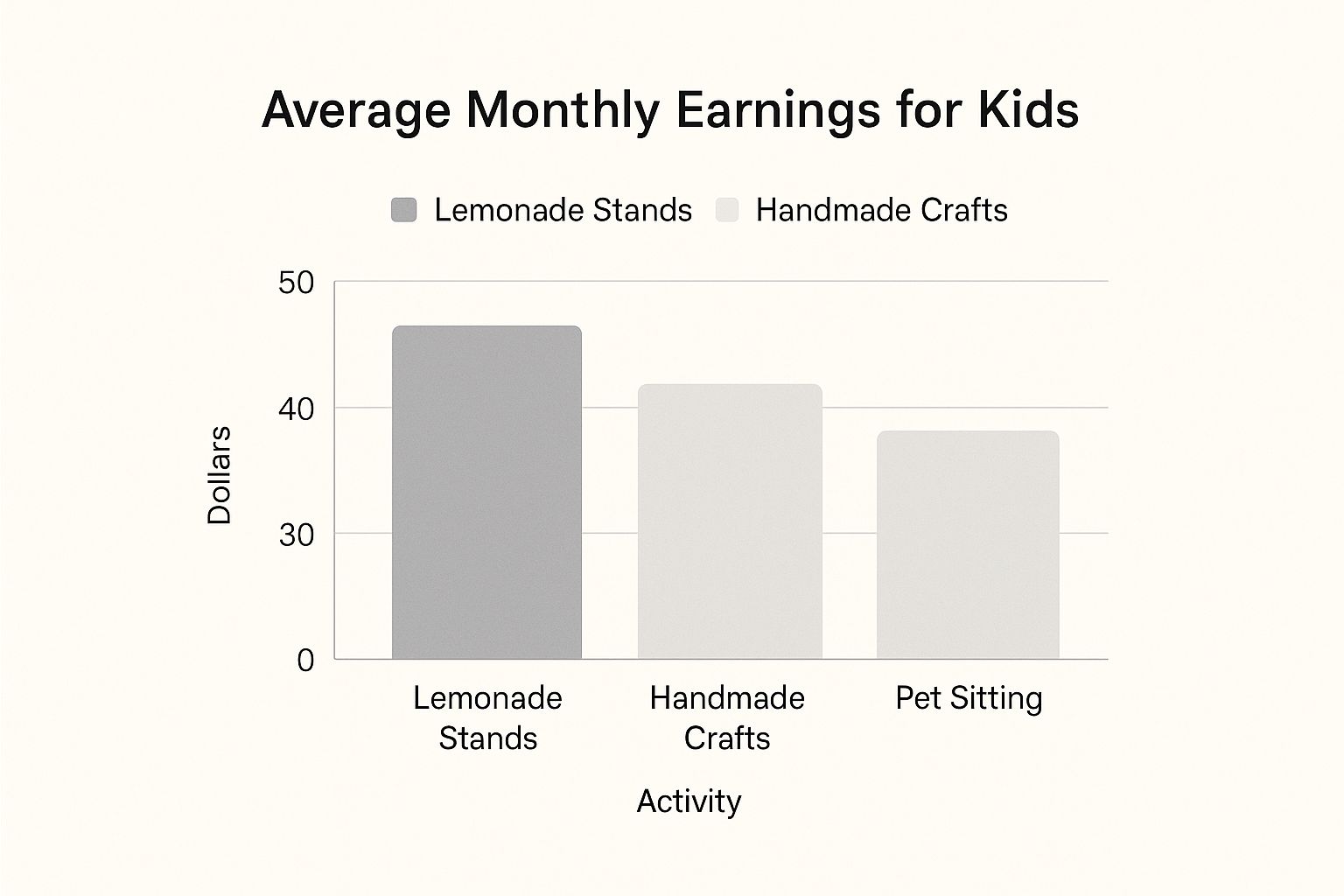

To give you a better idea of what's possible, let's look at how different jobs stack up. The chart below gives a snapshot of average monthly earnings for a few popular options.

As you can see, while a one-off project like a bake sale can bring in a nice chunk of change, it's the consistent, service-based jobs that tend to build a steadier income stream over time.

To help you brainstorm, I've put together a quick table that breaks down some popular earning methods, the skills they require, and what you can realistically expect to make.

Kid-Friendly Earning Methods at a Glance

| Earning Method | Skills Needed | Typical Earning Potential (Per Job/Hour) |

|---|---|---|

| Babysitting/Mother's Helper | Responsibility, patience, basic childcare knowledge | $10 – $20 per hour |

| Yard Work (Mowing, Raking) | Physical stamina, ability to follow instructions | $20 – $50 per yard |

| Pet Sitting/Dog Walking | Animal care, reliability, communication with owners | $15 – $30 per day/walk |

| Tutoring Younger Kids | Strong knowledge in a specific subject, patience | $15 – $25 per hour |

| Selling Crafts (Online/Local) | Creativity, craftsmanship, basic marketing | Varies greatly |

| Tech Support for Seniors | Tech-savviness, clear communication, patience | $10 – $20 per hour |

This table is just a starting point, of course. Your local rates might be higher or lower, but it gives you a solid idea of where to begin your research. The key is finding a good fit for your skills and schedule.

Key Takeaway: The absolute best way to make money as a kid is to find an overlap between your personal interests and a genuine need in your community. When you enjoy what you're doing, it stops feeling like a job and starts feeling like a hobby that pays.

I know getting started can feel like the hardest part. My advice? Talk to your parents first. Brainstorm your ideas with them. They can help you figure out how to safely market your services—maybe by making some simple flyers for the neighborhood or helping you set up a parent-supervised profile online.

The goal here isn't to become a millionaire overnight. It's to start small, build an excellent reputation one job at a time, and learn as you go.

Smart Business Ideas for Young Entrepreneurs

Ready to turn a great idea into real income? It all starts with one solid business concept you can really sink your teeth into. Whether you're someone who loves working with your hands or you're more of a tech whiz, there are legitimate opportunities out there you can start right now, often with just a little teamwork with a parent.

Let's look at some real-world ventures that are a step up from the usual lemonade stand. These are actual businesses you can launch, manage, and watch grow.

Hands-On Neighborhood Services

One of the fastest ways to start making money is by offering services that people in your own neighborhood genuinely need. You’d be surprised how many neighbors are thrilled to hire a young, reliable entrepreneur who does quality work.

Think about starting a professional pet-sitting service. It's a fantastic option. With a parent's help, you can design a simple flyer that clearly lists what you offer (like walking, feeding, and playtime) and your prices. Hand-deliver them to neighbors you trust and don't be shy about asking them to tell their friends. Feeling confident when you talk about your rates is important—practice your pitch with a parent a few times first!

Another tried-and-true winner is a mobile car washing service.

- Your toolkit: All you really need are some buckets, sponges, car-friendly soap, and soft towels. If your parents have a portable vacuum, you could even offer interior cleaning.

- Your first client: Practice on your own family's cars. This is a great way to get comfortable with the process and snap some impressive before-and-after photos for a portfolio.

- Setting your rates: A basic exterior wash might be $10-$15. A full-service wash that includes the interior could easily be $25 or more.

My Two Cents: Always be punctual. And try to do one small thing extra, like wiping down the tire rims. It’s those little details that make customers happy, turn them into regulars, and get them talking you up to others.

Digital Gigs for Tech-Savvy Kids

If you’re more at home behind a screen, there are tons of ways to earn money using your digital skills. These jobs are super flexible and can usually be done right from home (with your parents' oversight, of course).

For instance, you could offer to manage social media for a local small business. Lots of small shop owners are just too swamped to post consistently on Instagram or Facebook. You could step in and offer to create simple graphics, write captions, and schedule a few posts a week for a set monthly fee.

Selling your own unique creations online is another amazing route.

- The Marketplace: With a parent's help and permission, you can open a shop on a platform like Etsy. It’s a massive online market dedicated to handmade and custom goods.

- Your Products: What do you enjoy making? It could be anything from custom friendship bracelets and cool painted rocks to digital art downloads or personalized logos for gamers.

- Getting Started: Your main investment is your time and the cost of your materials. Make sure to take photos of your items in good, bright light so they really pop.

These online jobs don't just bring in cash; they also teach you incredibly valuable skills in marketing, customer service, and e-commerce.

For even more inspiration, check out these other fantastic ways for kids to make money that might just spark your next great idea. The secret is finding something that clicks with your interests, turning what you love to do into a real-deal business.

Managing Your Money Like a Pro

Earning your own money is an incredible feeling. But what you do with that money next is where the real magic happens. This is your chance to become the boss of your cash. It’s not just about counting what you’ve made; it’s about understanding where every dollar comes from and, just as importantly, where it goes.

Think of this as the foundation for a lifetime of smart financial decisions. The habit of tracking your earnings and spending is something that will serve you well long after you've outgrown your first gig. It’s also important to remember that the chance to learn these skills through your own small business is a genuine privilege.

While learning how to make money as a kid is often about choice and building good habits, it’s a very different story for many children around the globe. In 2024, nearly 138 million children were involved in child labor, where work is a necessity for survival, not an opportunity for growth. For these kids, earning money can come at the cost of their education and well-being. To better understand this global issue, you can read the full UNICEF report on child labor.

Choosing Your Money Tracking Method

You don’t need complicated software to get started. Honestly, the best method is the one you’ll actually stick with. Keep it simple.

Here are a few easy ways to get going:

- The Classic Notebook: A simple, dedicated notebook can be your first ledger. Just create two columns: "Money In" (Income) and "Money Out" (Expenses). It's low-tech, super effective, and very satisfying to fill out by hand.

- The Jar System: This is a fantastic visual method. Grab a few jars and label them for different goals like "Spending," "Saving," and "Giving." When you get paid, you physically divide the cash between the jars.

- A Simple Spreadsheet: With a parent’s help, you can set up a basic spreadsheet using a free tool like Google Sheets. This is a great way to get a comfortable with digital tools, and it does all the math for you—a huge plus.

Key Insight: Tracking your money isn't about restricting fun. It’s about giving yourself control. When you know exactly where your money is going, you can make way smarter decisions about how to use it.

Putting Tracking Into Practice

Let’s say you’re running a lawn-mowing business. This is where tracking changes everything.

You mow Mrs. Smith’s lawn and earn $30. Great! That goes straight into your "Income" column. But hold on—before that, you spent $5 on gas for the mower. That’s a business expense.

By logging both numbers, you instantly see your real profit is $25.

This simple bit of math is a total game-changer. It helps you understand the crucial difference between revenue (the total money you bring in) and profit (what’s actually left after your costs). This is the core of running any successful business, whether it's mowing lawns or a massive corporation. Building this habit now creates a powerful financial foundation you'll rely on for the rest of your life.

Making Sense of Taxes on Your Kid's Earnings

Alright, let's talk about the word "taxes." It can sound a little scary, but it's really just another piece of the money puzzle. Once your child starts making their own money, understanding the basics helps everyone handle this new income responsibly. We'll break it down so it's simple and stress-free.

The first thing to get straight is the concept of earned income. This is money your child gets for actual work they do—think mowing lawns, babysitting, or selling their cool handmade crafts. This is completely different from birthday money or a cash gift from Grandma, which the IRS views in a separate category. Knowing this difference is the very first step.

So, When Do We Actually Have to Deal With Taxes?

For most kids earning pocket money here and there, you probably won't have to worry about filing taxes. The IRS has specific rules, however, that trigger once earnings hit a certain amount for the year. The key number to remember applies to self-employment income, which is any money your child makes from running their own little business or doing freelance gigs.

Here's the rule of thumb: if your child's profit from self-employment adds up to more than $400 in a single year, you're required to file a tax return. Remember, profit is the money left over after you subtract all the business-related expenses. This is exactly why tracking those expenses we talked about earlier is so important!

Let's walk through a real-world scenario:

- Your daughter earned $700 from her summer dog-walking business.

- She spent $50 on supplies like flyers, dog treats, and a couple of new leashes.

- Her total profit is $700 – $50 = $650.

Because that $650 profit is more than the $400 threshold, this is a situation where you would need to report that income to the IRS.

A Quick Heads-Up: Tax laws can be tricky and they do change. This guide is meant to give you a solid starting point. I always recommend that parents chat with a qualified tax professional to get advice tailored to their specific family situation.

Your Best Friend at Tax Time: Good Records

The secret to making this whole process painless is being prepared. You don't need some complex accounting software; a simple spreadsheet or even just a dedicated folder for receipts is all it takes. Think of good records as your proof—they back up all your income and expenses.

Here’s a simple checklist of what to keep:

- An Income Log: This can be a simple notebook or a spreadsheet. For each payment, just jot down the date, who paid, the amount, and what the job was.

- All Your Expense Receipts: Hold onto every single receipt for things your child buys for their business. This includes everything from art supplies for a custom greeting card business to the gas used in the lawnmower.

- A Mileage Log: If you're driving your child to different jobs, keeping a simple log of the miles can sometimes count as a deductible business expense. It’s a great habit to get into.

By keeping these records organized throughout the year, you’ll do more than just make tax time easier. You'll give your young entrepreneur a crystal-clear picture of their business's financial health, which is a fantastic skill to build as they learn how to make money as a kid.

Supercharge Your Savings with a Roth IRA

Once you've started making money and keeping track of it, you get to take the next, most exciting step: making your money work for you. This is where you graduate from simply saving to actually investing. Let’s talk about one of the most powerful tools a young earner has: the Custodial Roth IRA.

Think of a Roth IRA as a special type of savings account with a serious superpower. The money you put inside can be invested, and here's the best part: all the growth it earns over the years can be completely tax-free when you pull it out in retirement. That is a huge, game-changing advantage.

Why Starting Young Is Everything

The real magic behind a Roth IRA is a concept called compound interest. This is the snowball effect in action—your investment earnings start generating their own earnings, and the whole pile grows bigger and faster over time. The more time your money has, the more powerful this effect becomes.

Starting as a kid gives you an almost unfair head start. Seriously. Even small amounts of money you contribute during your teenage years can grow into a shocking amount of wealth by the time you're ready to retire. It's the ultimate long game.

A small seed planted today can grow into a mighty tree over decades. That's exactly how a Roth IRA works for a young person. Just a few hundred dollars invested now could be worth tens of thousands—or more—by retirement.

To get a Custodial Roth IRA up and running, there are a few key things you and your parents will need to do together. It’s a team effort.

- You must have earned income. This is the number one rule, and it's non-negotiable. The only money you can put into a Roth IRA is money you've earned from a job—like your dog-walking business or craft sales. Birthday cash or allowance won't work.

- An adult needs to open it. Since you're a minor, a parent or guardian has to open the account for you. They'll act as the custodian, managing the account until you're legally an adult in your state.

- You can contribute up to your earnings. Once the account is open, you can deposit money up to the total amount you earned for the year. There's an annual cap set by the IRS, which is $7,000 for 2024.

A Real-World Look at Compound Growth

Let's paint a picture. Imagine you're 15 and you hustled all summer to make $1,000. You decide to put that entire $1,000 into your brand-new Roth IRA. Then you forget about it and never add another penny.

If that money grows at an average of 8% per year, how much do you think it could be worth when you turn 65? That single $1,000 investment could balloon into over $21,000. That’s the raw power of starting early.

The process of opening an account is pretty straightforward, but you definitely want to get it right. For a detailed walkthrough, our guide on how to start a Roth IRA for a child breaks down every single step for parents. This incredible financial tool helps turn the lessons from your very first job into a real foundation for lifelong wealth.

Answering Your Top Questions About Kids and Money

When your kid decides they want to start earning their own money, it’s exciting! But it also brings up a ton of questions for both of you. It's totally normal to wonder about the rules, the risks, and even the right way to ask for payment.

Let’s walk through some of the most common things parents and kids ask. Getting these answers sorted out from the beginning will help everyone feel more confident and prepared.

What's the "Official" Age My Kid Can Start Working?

This is probably the first question that pops into every parent's head. The official rule, according to the federal Fair Labor Standards Act (FLSA), sets the minimum age for most traditional jobs at 14. But—and this is a big but—that rule doesn't really apply to the kinds of kid-centric businesses we've been talking about.

The law carves out some major exceptions. In fact, there is no federal minimum age for a child to:

- Work in a business owned entirely by their parents (as long as it’s not a dangerous job).

- Do casual jobs like babysitting or delivering newspapers.

- Work as an actor.

- Help with minor chores around someone's home.

So, for those classic kid hustles—mowing lawns, walking dogs, selling crafts, or running a lemonade stand—there’s no magic age limit. The real deciding factor is your child's own maturity and whether they can handle the responsibility safely. You know your child best.

How Can My Kid Safely Earn Money Online?

The internet is full of possibilities, but we all know it comes with risks. Safety has to be the number one priority, period. The Children's Online Privacy Protection Act (COPPA) is a federal law that puts parents in the driver's seat, requiring your consent before any company can collect personal info from a child under 13.

Here’s how to navigate the online world safely:

- Be Their Co-Pilot: A parent absolutely must be involved. From setting up an account to messaging a customer, you should be there every step of the way. No exceptions.

- Use Parent-Managed Accounts: Thinking of opening an online shop? Most platforms, like Etsy, require the account owner to be 18 or older. This means you, the parent, will need to own and manage the shop for your child.

- Teach Them to Spot Scams: This is a life skill. Make sure they understand that any "job" asking for money upfront or promising way-too-good-to-be-true earnings is a red flag. Real opportunities don't ask you to pay them.

Our Family Rule: We never, ever share personal information like our home address, phone number, or school name online. All communication with customers runs through a parent’s email account. It’s just not negotiable.

How Do We Politely Ask to Be Paid?

Ah, the money talk. It can feel a little awkward at first, but learning how to handle it is one of the most valuable skills your child can develop. The secret is being clear and upfront from the very beginning.

Before any work starts, make sure everyone agrees on the price. Once the job is finished, a simple, polite script works wonders. Your child could say something like, "I had a great time walking Sparky this week! The total comes to $25. Is cash okay, or would you prefer another way?"

For the first few times, just having a parent nearby can give a kid a huge confidence boost. It’s great practice and teaches them to value their effort and communicate like a pro.

The information provided in this article is for educational and informational purposes only and does not constitute financial advice. We are not financial advisors. You should consult with a qualified professional before making any financial decisions.